Illustration for Dante Alighieri’s Commedia [Divina]: Inferno

Stoneleigh: Chris Martenson recently posted a rebuttal to the deflationist take on commodities - Commodities Look Set to Rocket Higher. In contrast, our deflationary view here at The Automatic Earth, written at the end of August, is encapsulated in Et tu, Commodities?. To recap, our position is that commodity prices are coming off the top of a major speculative episode and consequently have a very long way to fall.

That is how speculative periods always resolve themselves. We argue, however, that this does not mean commodities will be cheap, even at much lower prices than today, given that the implosion of the wider credit bubble will cause purchasing power to fall faster than price. This means affordability worsening even as prices fall.

To be clear, at TAE we define inflation and deflation as monetary phenomena - respectively an increase or a decrease in the supply of money plus credit relative to available goods and services. Mr Martenson begins his piece with:

Their argument is pretty clear cut: Because inflation is a function of available money plus credit (their definition), and because credit has fallen, deflation is what comes next.

We would point out that, according to our definition, credit contraction does not lead to deflation, it IS deflation by definition. What it leads to is falling prices, virtually across the board.

Mr Martenson points to three conditions which he argues would have to be met for commodity prices to fall, arguing that these are "all just versions of the old supply/demand argument for commodity prices, except that our consideration also includes the important element of the Austrian economic view of demand for money".

In this view, three things have to be true:

- Demand for commodities has to fall below supply. After all, as long as demand exceeds supply, prices will typically rise.

- Money, including credit that would normally be used to buy commodities, has to shrink. That's the definition of deflation that we're analyzing here.

- People's preference for money has to be greater than their preference for 'things,' with commodities being very obvious 'things.' That is, faith in money has to be there or people will prefer to store their wealth elsewhere.

Regarding the first condition, Mr Martenson has this to say:

A key component of the deflation argument is that with credit shrinking, demand will drop, leaving excess market supply that resolves with lower commodity prices.”

This does not represent our position, which is based on the powerful impact of bubble psychology, rather than on supply and demand. In contrast, we would argue that for commodity price to fall a long way, and very quickly too, it is not necessary for supply to exceed demand, especially by any significant margin.

Changes in supply and demand do not typically occur rapidly, but changes in perception certainly do, and it is perception that drives markets. If the fundamentals of supply and demand were responsible for setting prices, we would not see price collapses over a matter of months, yet this is exactly what we saw in 2008.

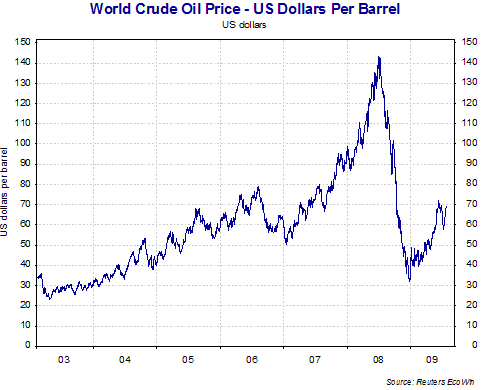

The dramatic move in 2008 from $147/barrel to under $35/barrel had essentially nothing to do with supply and demand, and everything to do with speculation shifting into reverse, in other words the implosion of a speculative commodity bubble.

The fact that the entire commodity complex showed essentially the same behaviour at the same time, and that financial crisis was becoming acute, strongly suggests that the fundamentals of any particular industry have little to do with prices in the short term, and that financial conditions are a major driver in their own right.

We do expect demand to fall, and for this to have a depressive effect on oil prices further into the future, but we do not expect this to be the primary driver of price collapse in the short term. Our view is that both demand and commodity prices will fall as a direct result of financial crisis, in the form of an acute liquidity crunch, and that prices will do so far more quickly.

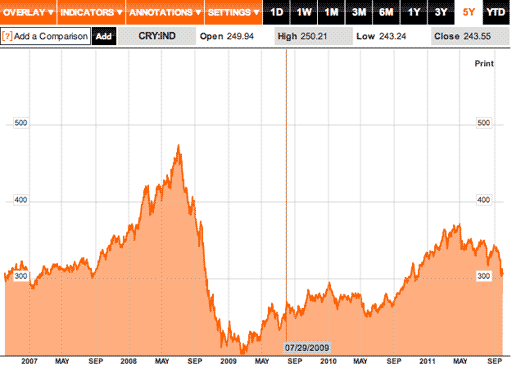

The real supply and demand economy responds over a much longer timeframe than financial effects. The ebb and flow of liquidity have been moving disparate markets in synchrony and we expect this to continue. See for instance the common May 2nd top in the S&P, the CRB Index and crude oil.

Speculation going into reverse should account for the majority of the downward price move we expect to see, which we anticipate will (temporarily) take prices below the 2008/2009 bottom. Since then, prices have once again been bid up on fear of shortages, as they were into the 2008 top. This is very typical for commodities.

Commodity bubbles form on the perception of imminent scarcity, which leads to additional money flooding into a sector on the grounds that future prices 'must rise', and that there are therefore profits to be made by betting on a rise. This response is accentuated where purchasing power is plentiful and leverage readily available, as during a period of credit expansion. The perception of near-term scarcity can then become a self-fulfilling prophecy.

Acute fear of shortages gets ahead of itself, driving prices to unrealistic heights in a classic Ponzi structure that will collapse once the Greatest Fool (or most aggressive speculator) has committed himself, and there is no one left to drive the trend further in that direction. The speculative premium disappears, and then opposite dynamic asserts itself - speculation that prices will now fall, which becomes another self-fulfilling prophecy.

Speculative reversals are thus followed by a temporary undershoot, as we saw in 2008. Prices fall to well below where the fundamentals would place them - in the case of commodities perhaps to the cost of the lowest price producer.

Mr Martenson says:

If it costs $70 - $80 to produce a new barrel of oil, the price cannot fall much below that for very long.

Production costs are very likely to fall in a deflationary environment, albeit not nearly as quickly as oil prices, meaning that many suppliers would be squeezed. The cost of the lowest prices producer could end up considerably below where it is today. Prices could temporarily undershoot even this level.

We have seen in North American natural gas markets, in the context of shale gas, that production can temporarily be maintained at unprofitable levels. We do not expect a downward price spike to extremely low levels to be maintained for long, however, because production costs falling more slowly than price will eventually drive producers out of the market, reducing the (temporary) excess of supply.

Approaching scarcity leads not to a one way trip to the moon in price terms, but to an exaggerated boom and bust dynamic, which we have seen in force since 2006. The fundamentals interact with perception, and the inevitable resulting herding behaviour, in complex, yet probabilistically predictable, ways. Movements in both directions can be large and rapid. Volatility, in response to fear and uncertainty, is the name of the game.

Markets are creatures of positive feedback, and commodities are no exception. It is not enough to understand the fundamentals. One must also understand how those fundamentals will interact with human nature at a collective level. As in quantum physics, the observer and the system are not independent. The view of prices as a function purely of supply and demand rests on the notions that markets are rational, efficient and omniscient, and that human effects are an irrelevant external factor.

We maintain that this view is a completely inaccurate description of reality. Human actions, particularly the collective actions of herding behaviour, cannot be assumed away - they must be viewed as an inherent, and indeed vital, component of the system. Human beings chase momentum, often in the absence of any real information at all. They jump en masse on to passing bandwagons on the assumption that someone must know what they are doing.

We regard markets as fundamentally irrational and driven by emotionally-grounded perception, not by reality. They exhibit an eternal tug-of-war between collective greed and fear that expresses itself in fractal patterns. This lends itself to technical analysis (based on Elliottwaves), but not of the kind mentioned by Mr Martenson in his article. Elliottwaves identify and rank different unfolding possibilities for market action. There are always many possibilities as fractals unfold at all degrees of trend simultaneously.

The highest ranked option will be the one that satisfies the greatest number of guidelines while violating no rules, but it is not always the highest probability option that plays out. What Elliottwave analysis does is to indicate higher and lower probability time periods for trend changes, and boundaries for interpreting subsequent price action in the context of different possbilities, providing advance warning of potentially significant moves. In conjunction with contrarian sentiment indicators, it is a powerful, if inherently probabilistic, tool.

Continuing on the supply and demand theme, Mr Martenson comments on the apparently insatiable demand of India and China:

What's new in this story today is the emergence of a couple of new economic powerhouses with billions of citizens as new participants at the resource table....We're seeing exactly what you would expect from a major economy expanding like crazy: a rapidly growing, or, shall we say, exponentially increasing hunger for natural resources....Perhaps a slump in the Western economies will suddenly flood the world with enough resources to cause a commodity crash, but perhaps not....

....So on the first deflationist point that supply of commodities will soon greatly exceed demand, I have to conclude that until and unless we see China's and India's economies fall off a cliff, the impact of bringing an additional 2.5 billion consumers to the global buffet of natural resources will provide ample pressure to prevent a sustained crash in prices. Perhaps we'll experience a short-term correction, especially if the Fed is stingy with its still-unannounced QE III program, but a long-term crash seems highly unlikely.

We have said for some time that we do not expect the Fed to provide a QE3. Even if it were to attempt to do so, we are of the opinion that it would be a miserable failure. The previous rounds of quantitative easing occurred against the backdrop of a supportive rally, and rallies are kind to central authorities by making their actions appear effective. Rallies unfold on a temporary resurgence of optimism, which leads people to extend credence to their leadership.

This suspension of disbelief allows interventions to achieve apparent traction. Once this supportive psychological milieu gives way, however, and the larger down-trend is back in force, which it has been since May 2nd, optimism rapidly dissipates and disbelief reasserts itself. The actions of central authorities under such adverse conditions are very likely to appear incompetent and useless. Kicking the can further down the road under such circumstances will be exceptionally difficult.

Exponential growth, particularly in the form of a dramatic parabolic rise, as we have seen in India and China, is the hallmark of a bubble living on borrowed time. Exponential growth curves end in collapse, and those in India and China will be no exception.

In other words, it is not just western economies that are poised to experience a sharp reversal of fortunes, but the rapidly growing BRIC countries as well. They too have lived through massive credit expansions, with concommitant build up of unpayable debt, and like western countries, their bad debts are set to messily implode in credit crunch and demand crash.

They have focused on building an export economy during their expansion phase, and have benefited from a global consumption boom, but that is coming to an end. Much of the export capacity, built on bad debt, will prove to have been wasted capital as consumption collapse, and with it export markets.

As empires in the ascendancy, the difficulties of India and China are likely to be less intense and more transitory than the old imperial centres moving into decline. For this reason, their domestic demand is likely to recover far more quickly, although the death of their export markets will be an enduring factor that could yet take considerable time to overcome.

If by the time Indian and Chinese domestic demand begins to recover enough to overcome the loss of export-driven demand, global energy supply has been squeezed by low prices, we could expect a major price spike in the next few years on the continuation of the exaggerated boom and bust cycle continues. A potential future resource grab would accentuate this considerably. Prices for commodities such as oil could therefore bottom relatively early in this depression.

We at TAE are not failing to recognize in our arguments either resource limits or recent demand history in the BRIC countries. However, we are firmly of the opinion that it is primarily money rather than natural resources that we and others will find ourselves acutely short of over the next few years. Beyond that, we can expect resource limits to reassert themselves. In volatile times, different factors can become limiting at different times, and relative values can change almost overnight. The key is to anticipate these moves, which is far more challenging than merely extrapolating current trends into the future, as many analysts commonly do.

The second condition Mr Martenson cites is that money, including credit that would normally be used to buy commodities, has to shrink. His objection is that:

This explanation is especially problematic for me when it is used in an overly broad way by lumping all credit market debt into a single spot and then saying, "There. Look. It's fallen. Credit is down, and that's deflationary."....(Hey, credit has to be paid back at some point, right? So it's roughly neutral over the long haul.)

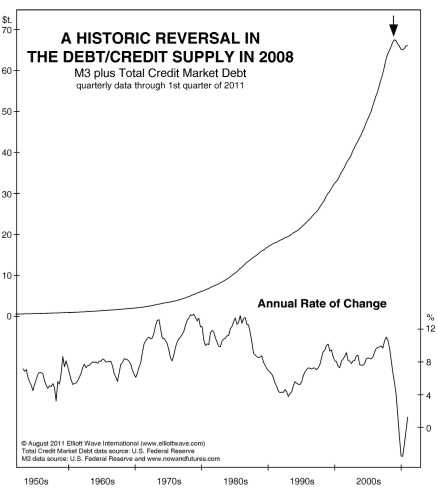

As I pointed out previously, credit contraction is not deflationary, it IS deflation by definition. We not only regard this as inevitable, we would argue that it is already well underway. Credit began to contract in 2008 for the first time since WWII. Although it has bounced back to some extent with the rally from March 2009, it has not regained its peak. Now that the larger downward trend has resumed, we can expect credit contraction to reflect this, following a time lag for the contraction to appear in the data.

To argue that credit is neutral, since it has to be paid back at some point, is to miss an enormous impact between the begging of a credit expansion and the end of its aftermath. Credit has the effect of bringing demand forward and then crashing it thereafter. The effect may be neutral if one takes a sufficiently long term view, but that view would have to cover several decades of tremendous boom and bust. Averaging that out over such a period of time would be to miss the largest factor influencing commodity prices for a century, or indeed perhaps in history, and that seems highly counter-productive to the effort of understanding what is happening and why, and how it will play out from here.

The collapse of the Ponzi credit expansion of the last thirty years will crash the effective money supply, given that credit represents the vast majority of that money supply today. Credit represents excess claims to underlying real wealth. During the bubble expansion phase, the increase in claims to wealth greatly outstrips any growth in real wealth. The flip side of credit expansion is debt, hence during a credit expansion, debt becomes less and less well collateralized, and the real economy more and more hollowed out as a result.

The blinding optimism characteristic of expansion keeps people from noting this fact until it is far too late to prevent a debt implosion that will proceed at least until the small amount of remaining debt is acceptably collateralized to the few remaining creditors.

The excess claims that credit represents will be largely eliminated under this scenario. Confidence and liquidity are equivalent. When confidence evaporates, as it does on the recognition of of an unpayable debt predicament, liquidity will shrink proportionately. This cannot help but reduce purchasing power. In fact, 'reduce' is a considerable understatement from the perspective of the vast majority of people.

The depression conditions that result from the bursting of a large bubble can virtually eliminate purchasing power for many, or perhaps most. Since the aftermath of a bubble is roughly proportionate to the excesses that preceded it, and this has been the largest bubble in human history, we can expect an extremely severe depression to follow.

Mr Martenson distinguishes between the effect of credit expansion and contraction on financial assets versus the effect on the consumer price index (CPI), suggesting that the two are independent, and that effects in the financial sector have little effect on the real economy:

The trouble I have with this view is that not all credit has the same impact on demand. Some credit leads to demand that directly impacts the CPI (inflation), and some does not. When we are talking about inflation, what most people care about is the price of things they use or consume (cars, food, gasoline, health care, houses, etc.), rather than financial instruments or paper assets (stocks, bonds, derivatives, etc.)....Whether credit-default swaps (CDS), traded within and among the shadowy world of purely financially motivated entities, are trending up or down in price has almost zero impact on the price of molybdenum or corn.

It is difficult to imagine how the disappearance of access to credit, combined increased debt burden on spiking interest rates, skyrocketing unemployment, falling (and highly insecure) incomes, loss of pensions and other entitlements, loss of investment value as asset prices collapse, and loss of savings to a systemic banking crisis, all of which are typical of deflationary episodes, could possibly fail to have a dramatic impact on people's collective purchasing power.

The tremendous potential impact on purchasing power in turn cannot help but impact upon the ability of people to convert their wants into what they can actually afford. It is not that people will no longer want commodities, or many other goods and services, but that they will not be able to afford them in anything like the previous quantity. Demand is not what one wants, but what one is ready, willing and able to pay for. For a time, supply will be geared to the previous level of demand, leaving a substantial surplus that should weigh on prices for a significant period of time.

The odds of people being able to pay what they once could for commodities under such circumstances are effectively nil. It is as if we were playing a giant game of musical chairs, where there is only one chair for every hundred people playing the game. When the music stops, most will be out of the 'game' after a short but chaotic wealth grab.

If we see a resurgence of demand in BRIC countries sooner rather than later, perhaps accompanied by future price spikes and resources grabs, the firming up of price support at that time would almost certainly price a large number of people in depression-gripped western countries out of the commodity market entirely, since their purchasing power would not have recovered. This would be a recipe for significant socioeconomic unrest in a large part of the world.

Mr Martenson asserts that:

"There's been $3 trillion of new credit created in the consumptive portion of the economy since the start of the financial crisis in 2008, and it's almost entirely thanks to government borrowing. Not too shabby.”

We would argue that demand supported by government borrowing is entirely artificial, amounting to a further episode of bringing demand forward at the expense of the future. This cannot be realistically argued to be a positive effect on the global economy going forward, as it will result in a further paucity of future demand, and consequent downward price pressure. The future pain in store for suppliers, and the probability of a consequent future supply squeeze, are amplified by this action.

Mr Martenson's third condition involves the demand for money versus the demand for tangible stores of value. He suggests that we should bear in mind the shift from perceived value of paper assets towards commodities and other real assets. While we would agree that over the long term such a shift will indeed take place, our view is that we are about to see a sharp reversal of this trend in the short term. Cash is king in a deflation.

In our view, we are going to see a rapid and substantial shift towards a desire to maintain liquidity, on the grounds that liquidity represents uncommitted choices, and that people will be anxious to maintain their freedom of action to respond to massive uncertainty. This is likely to last into the medium term (ie probably a number of years). It is absolutely vital to anticipate this type of trend change. Extrapolating past trends forward is simply not good enough.

Mr Martenson points to measures of monetary expansion as evidence that deflation is not in fact occurring:

There is absolutely nothing deflationary in the M2 chart. It is exactly what we would expect to see from a culture that placed a man at the monetary helm on the basis of his promise (Jackson Hole, 2002) to run the printing presses if deflation came knocking.

We would argue that expansion of narrow measures of money are largely irrelevant, since they are dwarfed by credit contraction over the same period, and deflation is defined as contraction in the supply of money plus credit. Also,it cannot be ignored that the velocity of money is plummeting, which is characteristic of the developing economic seizure we anticipate in a depression. This will resemble Dante's Ninth Circle of Hell - a frozen lake where nothing moves.

Illustration for Dante Alighieri’s Commedia [Divina]: Inferno

To cast a different light on the purported expansion of the tiny (relative to credit) 'money' fraction of the effective money supply, consider that the expansion of M2 likely reflects not traditional money printing, but capital flight from Europe in response to the eurozone crisis.

Larry Kudlow for the National Review -

The Deflationary M2 Explosion:Amidst the financial flight-wave to safety, with stocks plunging, gold soaring, and Treasury bond rates collapsing — and all the European banking fears which go with that — there’s an important sub-theme developing: An almost-forgotten monetary indicator, M2, which is mostly cash, demand-deposit checking accounts, savings deposits, and retail money-market funds, has been soaring.

According to the St. Louis Fed, M2 is up 24.2 percent at an annual rate over the past two months. Almost out of the blue, that comes to a near $500 billion increase. In rough terms, the M2 explosion breaks down to $165 billion in demand deposits and $335 billion in savings deposits.

What’s going on here? There’s a flight to government-guaranteed accounts. Some people believe Europeans are withdrawing from their own banking system and parking their money in the U.S. banking system, guaranteed by Uncle Sam. Kelly Evans reports in her Wall Street Journal column of a $30 billion outflow from equity mutual funds that has probably gone into cash.

This is a very disconcerting development. Normally, big M2 growth would signal a faster economy, and maybe even higher inflation. But as economist Michael Darda points out, the velocity, or turnover, of money seems to be plunging.

"The recent pickup in broad money in the U.S. looks like a dash for risk-free cash assets," writes Darda. He also notes that widening corporate-credit risk spreads and shrinking government-bond rates signal a recession risk, not a coming boom.

So contrary to monetarist theory, the M2 explosion seems more closely related to a deflation/recession risk. Economist-blogger Scott Grannis writes, "The recent growth of M2 surpasses even the explosive safe-haven demand for money that accompanied 9/11 and the financial crisis of late 2008. Something big is going on, and it can only be the financial panic that is sweeping Europe as money flees a banking system that is loaded to the gills with PIIGS debt."

Grannis concludes, "In short, it looks like there is a run on the European banks and the U.S. banking system is the safe-haven of choice.“

The game changed on May 2nd. We need to consider where we are now headed and why, and the answer is a long way from anything remotely resembling our comfort zone. The sea-change involved in the resumption of the credit crunch cannot be underestimated.

The Automatic Earth

Donate to our Summer Fund Drive

Time to stop torturing Greeks

by Mary Ellen Synon - Daily Mail

You've already read it on the news pages, but I wonder if you've spotted the puzzle: the Greek government has confirmed it will miss its 2011 deficit projections, and GDP will fall by over 5 percent this year and by 2.5 percent next year. The news has rattled the financial markets.

Got it? The puzzle is why the markets were in anyway surprised by any of that: of course the deficit projections have been missed, and of course the GDP will go on falling. That is all that could happen in Greece under the EU regime of extreme forced deflation. What else were the markets expecting from Athens -- fiscal rectitude and growth while the world heads into recession and Greece is trapped in a deadly currency union?

There is another puzzle, too, and that is why the Greek prime minister can only look at the suffering of his country under the Brussels-enforced scheme and instead of rebelling and saying 'Enough!' he just goes on with the abasement of his nation. He looks at the ruin of debt, unemployment, and misery his country's agreement to 'save the euro' has brought, yet all he can say is: 'We will be unswerving in our goal: to fulfill all that we have promised to ensure the credibility of our country.'

So, to save his country's 'credibility' in the eyes of the ideologues of Brussels -- because heaven knows he is not saving its credibility in the eyes of international investors -- Papandreou is willing to oversee the destruction of his country's economy.

It's getting spooky, as if the man's brain has been taken over and reprogrammed by a cult. What he needs to say is: 'Enough of this torture. Time to leave the euro.'

At least, that is what Charles Dumas of Lombard Street Research is saying this morning, and I'd say he is dead right: 'How long before the malignant euro-fanatics give up on the nightmare of a unified Europe? Most previous attempts to unify Europe have led to mass murder. It is time for Euroland authorities to return to reality and give up their deluded visions, rather than torture Greeks.'

Why Europe Is Right and Obama Is Wrong

by Michael Sauga - Spiegel

US President Barack Obama has recently suggested that Europe must take on more debt to stimulate the economy. Such reliance on cheap money, though, is what got us into the current crisis in the first place -- both in Europe and in the US. America's problem isn't too little money. It's a lack of competitive products.

"The Broken Jug" is one of the most frequently performed plays in German theater. With the village judge Adam, who passes judgment on a crime he committed himself, Heinrich von Kleist created one of the classic comedic figures of world literature.

US President Barack Obama currently seems to be portraying a modern version of Kleist's village judge. He is increasingly vocal in his criticism of Europeans for supposedly having exacerbated the ongoing economic crisis with their caution. His audience, however, seems to sense that the plight Obama is lamenting originated in his own country.

It stems from a doctrine that has dominated economic thought for the last two decades and consists of two elements: turbo-capitalism, whose only tenet is that any regulation of financial markets inhibits growth, and its more accommodating but no less dangerous brother, turbo-Keynesianism.

American economists, central bankers and fiscal policy makers have reinterpreted British economist John Maynard Keynes's clever idea that government spending is the best way to counteract a serious economic downturn -- and have turned it into a permanent prescription. In their version of the Keynesian theory, declining growth or tumbling stock prices should prompt central banks to lower interest rates and governments to come to the rescue with economic stimulus programs. US economists call this "kick-starting" the economy.

Laying the Groundwork for the Next Crash

The only problem is that this method of encouraging growth has not stimulated the US economy in recent years, but in fact has put it on a crash course. From the Asian economic crisis to the Internet and subprime mortgage bubbles, economic stimulus programs by monetary and fiscal policy makers have regularly laid the groundwork for the next crash instead of encouraging sustainable growth. In the last decade, the volume of lending in the United States grew five times as fast as the real economy.

Cheap money created the fertilizer for the excesses of the US financial industry. Low interest rates seduced mortgage providers into talking even the homeless into taking out mortgages. And the same low rates made it easier for investment banks and hedge funds, using increasingly risky loan structures, to transform the once-leisurely insurance and bond markets into casinos.

Now the bubble has burst. This has not, however, prompted the US government to conclude that its prescriptions could have been wrong. On the contrary, now it wants to increase the dose. Obama plans to follow the largely unsuccessful 2008 economic stimulus program with a new program this year. Meanwhile, Federal Reserve Chairman Ben Bernanke says that he intends to flood the economy with cheap liquidity -- for years, if necessary.

The real problem, though, is a different one. The US economy doesn't lack money. Rather, it lacks products that can compete in the global marketplace. The country has a deep trade deficit, yet the Obama administration is borrowing money at the same rate as near-bankrupt Greece.

A Rapid End

Not even the financial sector, with its affection for cheap money, believes that this is the way to guide the United States out of the crisis. When the Fed recently announced a new version of its low-interest-rate policy, with the snappy name "Twist," it led to a sharp decline in the stock market instead of the expected boost.

It is all the more disconcerting that Obama is now recommending that the Europeans emulate his failed strategy. To save the euro, the president has proposed that Europe take on more debt to augment their bailout funds and stimulate their economies. Like a doctor caught prescribing performance-enhancing drugs, Obama has not chosen to cease his activities. Rather he is trying to ensure that as many people as possible have access to his wares.

The fact that Europeans are unwilling to comply with Obama's strange logic gives reason for hope. It makes no sense to pile up more and more debt on already unstable piles of debt. The world doesn't have too little debt, but too much. Obama should retract his advice, or he might end up like the village judge in Kleist's comedy. When his deception was discovered, he was forced to flee and his days as a judge came to a rapid end.

Germany won't give more to bail-out fund

by Skynews

German Finance Minister Wolfgang Schaeuble has ruled out Germany contributing any more money to the beefed-up EU bail-out fund than the 211 billion euros ($A294.51 billion) approved by parliament.

'The European Financial Stability Facility has a ceiling of 440 billion euros, 211 billion of which is down to Germany. And that is it. Finished,' he told the magazine Super-Illu in an interview published on Saturday.

He also suggested the European Stability Mechanism, which is due to replace the EFSF by 2013 at the latest, would be smaller. 'Then it will be only a matter of 190 billion in total, for which we will be guarantors, including interest,' he explained.

Germany's lower house of parliament, the Bundestag, on Thursday approved the beefing up of the eurozone bailout fund, which cleared its final hurdle on Friday when it was rubber-stamped by the Bundesrat (upper house).

The vote had been seen as a crucial test of Chancellor Angela Merkel's authority amid fears of a backbench rebellion. However she secured an overwhelming majority of her own deputies to back the move. A majority of Germans (58 per cent) consider it was a mistake to boost the EFSF, according to a poll to be published on Sunday in the weekly Bild am Sonntag.

German Foreign Minister Guido Westerwelle said he wanted the debt-ridden countries put under tighter surveillance in an interview given to Saturday's Sueddeutsche Zeitung. 'A right to scrutiny and make recommendations isn't enough. The states, which in the future will benefit from the solidarity of the rescue fund, should give the European authorities the right to intervene in their budgetary decisions,' the minister said.

Protectionism beckons as leaders push world into Depression

by Ambrose Evans-Pritchard - Telegraph

The world savings rate has surpassed its modern-era high of 24pc. This is the killer in the global system. It is why we are at imminent risk of tipping into a second, deeper leg of intractable depression.

The International Monetary Fund (IMF) expects the savings mountain to rise yet further next year as the governments of Europe, Britain, and the US tighten belts, in unison, by up to 2pc of GDP. This is double the intensity of the last big synchronized squeeze in 1980.

They will do so before the private sector is ready to grasp the baton, and without stimulus from the trade surplus states (Germany, China, Japan) to offset the contraction in demand. Put another way, there is a chronic lack of consumption in the world. "This probably comes as a surprise to most people, gorged on propaganda about excessive debt and the need for retrenchment," said Charles Dumas from Lombard Street Research.

The inevitable outcome of one-sided austerity polices in the Anglo-sphere and Club Med is a self-feeding downward slide for the whole global system, a variant of 1930s debt-deflation. "Excess savers refuse to acknowledge that if world savings are demonstrably too high, healthy recovery depends on the surplus countries saving less," he said.

Mr Dumas said China's "grotesque and destructive" policies of over-investment (50pc of GDP) and under-consumption (36pc of GDP) are unprecedented in history, but at least China's currency advantage is being eroded by wage inflation.

His full wrath is reserved for the "fallacious and malignant policies" of Angela Merkel and Wolfgang Schauble in Germany. They are enforcing a Gold Standard outcome on the whole eurozone. "Suffused with self-righteousness, they insist that the imbalances must be put right only by deficit-country deflation."

The sheer scale of global imbalances is made clear in a paper by Stephen Cecchetti at the Bank for International Settlements. His paper contains a chart showing that combined surplus/deficits reached 6pc of world GDP in the boom, far beyond the extremes that led to the US losing patience in 1985 and imposing the Plaza Accord. The gap narrowed post-Lehman but is widening again.

Money flows are even more out of kilter. Cross-border liabilities have jumped from $15 trillion to $100 trillion in fifteen years, or 150pc of global GDP. This creates a very big risk.

"Gross financial flows can stop suddenly, or even reverse. They can overwhelm weak or weakly regulated financial systems," said Mr Cecchetti. Well, yes, this is now happening. Did anybody think about this when they unleashed globalisation with its elemental deformity, free trade without free currencies?

The self-correction mechanism is jammed. China holds down the yuan against the dollar through a dirty peg. Germany and its satellites hold down the D-mark against Club Med covertly through the mechanism of EMU.

This outcome in Europe is not deliberate (I hope); it is not a German plot; it is the unintended effect of a currency union created by ideologues against Bundesbank advice, and which has calamitous implications for German foreign policy and for Latin social stability.

My sympathies go to the hard-working citizens of Germany, Spain, Italy, Portugal, and Ireland for being led into this impasse by foolish elites. A global system biased towards export dumping has had unhappy effects on the US, UK, and Club Med. These countries have faced a Morton’s Folk over recent years: an implicit choice between job losses at home, or accepting credit bubbles to mask the pain.

They chose bubbles. That was a mistake. This strategy of buying time cannot safely be repeated because fiscal woes are already near "boiling point", in the words of the BIS. “Drastic improvements will be necessary to prevent debt ratios from exploding," it said.

Bank of England Governor Mervyn King called recently for a "grand bargain" of the world's major powers to break the vicious circle and ensure that the burden of adjustment does not fall on debtors alone. "The need to act in the collective interest has yet to be recognised. Unless it is, it will be only a matter of time before one or more countries resort to protectionism. That could, as in the 1930s, lead to a disastrous collapse in activity around the world," he said.

We are not there yet, but a global double-dip would take us to the edge. US democracy cannot allow America’s precious stimulus to leak out to countries that have bent their exchange rates, tax systems, and industrial structures towards predatory export advantage. It cannot let broad (U6) unemployment ratchet up to 20pc or more. If the White House will not do it, Congress will. Capitol Hill is already launching its latest bill to label China a currency violator, and open the way for retaliatory sanctions.

"They get away with economic murder and thus far our country has just said, 'Oh, we don't care. This legislation will send a huge shot across China's bow,” said Senator Chuck Schumer. The risk – or solution? – is that the US will opt for a variant of Imperial Preference, the pro-growth bloc created behind tariff walls by the British Empire with Scandinavia, Argentina and other like-minded states in 1932. This experiment has been air-brushed out of history by free trade hegemonists.

One can imagine how this might unfold. North America would clamp down on dumping, at first gingerly, before escalating towards a cascade of Smoot-Hawley tariffs and barriers. Mexico and Central America would join. Brazil and Mercosur would find it irresistible because that is where the demand would be, and BRIC solidarity would wither on the vine.

By then you would have the US recovering behind its wall, while surplus states were recoiling from severe shock. Britain would face the moment of truth, offered salvation in the `Pact of the Americas’ or slow asphyxiation by trade ties to EMU’s deflation machine. Portugal and Spain would face the same fateful choice. This is how the EU might end.

Ultimately, America would get its way. Korea and the Asian Tigers would come knocking. The austerity brigade and mercantilists would be shut out until they capitulated. The rules of world trade system would be redrawn.

The IMF's Christine Lagarde understands the risks intuitively. The global economy is entering a "dangerous new phase", she warns. Leaders must prepare for "bold and collective action to break the vicious cycle of weak growth and weak balance sheets feeding negatively off each other". Central banks must stand ready to "dive back into unconventional waters as needed."

But how many infantry divisions does the IMF command, to paraphrase Stalin? Power resides in the G20, where debtors and creditors have radically contrasting views. The body cannot even start to offer a solution.

A US double-dip is not yet a foregone conclusion. America’s M3 money supply is last growing decently again at 5.6pc, which would in normal circumstances signal some recovery next year. The latest GDP and confidence data in the US have not been as bad as feared.

Ajay Kapur from Deutsche Bank said investors have to decide whether the market slump of recent weeks is a “panic like the LTCM sell-off in late-1998 that proved to be a great buying opportunity, or the first leg in what could eventually be a pervasive global recession. We believe it is the latter.”

He said the triple warnings from US leading indicators (ECRI, the Philly Fed’s 'Anxious Index', and the earnings revision index) all point to recession, while China is “probably over-tightening” into a global slump.

In Europe, policy is still on deflationary settings, with Italy and Spain having to tighten fiscal yet further to meet their budget targets. The European Central Bank is overseeing a collapse in real M1 deposits in Italy of around 6pc, annualized over the last six-months.

Michael Darda from MKM Partners said the ECB has made such a hash of monetary policy that nominal GDP for the whole eurozone may even start to contract. That is astonishing. If correct, there is no hope of averting a debt spiral in Italy and Spain. Any such outcome will test the EU’s bail-out machinery to destruction within months. Mr King’s “disastrous collapse” is staring policy-makers in the face.

If it doesn't do something about its underwater mortgages, America could sink without trace

by Heather Stewart - Observer

Stimulating the economy is all very well in the short term. But the national legacy of unpayable property debt will weigh the US down for years

It's now more than six years since Alan Greenspan, in the days when he was still known as the "maestro" of the world economy, conceded that there might be a little "froth", perhaps even a few "local bubbles", in the American housing market.

Subsequent events showed that he was a master of understatement, but not of much else. The sub-prime frenzy, which had seen cut-price loans to borrowers with dodgy credit histories squeezed through the slice-and-dice operations of Wall Street banks and sold on as top-quality investments, had helped to inflate an almighty bubble right across the US. When home prices started to decline, it triggered a worldwide credit crunch and what became known as the Great Recession; but it also took a painful toll on American society.

House prices have bounced back marginally from the depths of 2009, but they remain more than 30% below their peak. In some cities, where the boom was at its wildest, prices have fallen even further. In Las Vegas, for example, homes bought at the height of the sub-prime frenzy are now worth 59% less than their purchase price. So it's not surprising that more than one in five mortgage-holders are in negative equity, and many thousands of Americans have lost their homes.

Even the merest glimpses of Washington, caught between the IMF's glass-and-steel headquarters and the brownstones of Georgetown on a week-long visit last month, revealed a much larger than usual number of rough sleepers and vagrants huddled in doorways or begging on street corners – just the most visible manifestation of the ongoing social and economic crisis.

And while the world's eyes are on Athens, where state employees are facing yet another pay cut to satisfy the demands of the international bond markets, life on Main Street, USA is as tough as it has been in many years. The stagnant housing market continues to erode families' wealth and saddle them with ever more unpayable debts.

President Obama's ambitious jobs package, announced last month, is a valiant attempt to tackle the recalcitrant problem of unemployment, which remains above 9%. But even if he manages to get the plan past a ferociously partisan Congress, where his proposal to increase the marginal tax rate for millionaires has been described as "class war", it's unlikely to deliver a permanent solution to the economic malaise unless the housing market can be stabilised and the legacy of mortgage debt resolved.

Ben Bernanke at the Federal Reserve is trying to do his bit: Operation Twist, his latest wheeze, is directly aimed at driving down long-term interest rates and making mortgages more affordable, while the Fed is also continuing to invest in mortgage-backed securities to stop the credit markets drying up.

But the Fed's powers are limited, especially with conspiracy-minded Republicans breathing down Bernanke's neck. Just as in poor old Greece, the underlying problem in the US housing market is that the debts run up in the years of plenty will be a millstone around the neck of the economy for many years – and may ultimately be impossible to repay.

Even the IMF, hardly known as a champion of aggressive government intervention, said in its latest world economic outlook that Washington should try to find ways of writing down the value of some of these overblown loans.

"The large number of 'underwater' mortgages poses a risk for a downward spiral of falling house prices and distress sales that further undermines consumption and labour mobility," it warned, calling for courts to be allowed to write off a proportion of mortgages where borrowers have got themselves in trouble; for the taxpayer-backed mortgage guarantors Fannie Mae and Freddie Mac to encourage writedowns; and for an extension of state-level programmes to support troubled homeowners.

Each of these would be controversial, and they carry a risk of "moral hazard": the fear that reckless borrowers will in future feel they can take on eye-watering loans and assume the state will bail them out. But the alternative may be years of stagnation. Just as in Europe, pumping up short-term demand is fine, but tackling the legacy of a decade-long credit glut must be the starting point for stabilising, and ultimately rebuilding, the American economy.

Eurozone fix a con trick for the desperate

by Wolfgang Münchau - FT

We are now in the stage of the crisis where people get truly desperate. The latest crazy idea, which is being pursued by officials, is to turn the eurozone’s rescue fund into an insurance company, or worse, a collateralised debt obligation, the financial instrument of choice during the credit bubble. This is the equivalent of putting explosives into a can, before kicking it down the road.

To illustrate the danger of the CDOs as a solution to the eurozone crisis, it is important to recall a few facts about what happened during the credit bubble. CDOs lured investors to put money into mortgages. The CDOs themselves had triple-A credit ratings, even though they invested in bad assets.

What at first appeared to be a violation of the laws of economics, physics and logic, ultimately had a simple explanation. The overall risk of the CDO was lower than the sum of its parts. When the bubble burst, governments stepped in and prevented a catastrophe.

So why use such a toxic instrument to construct a product to save the eurozone? The current lending size of the European financial stability facility (EFSF) is €440bn, which is equal to the guarantees given by the 17 eurozone member states. If you want to leverage the CDO without increasing the liabilities of governments, then this €440bn would become the equity tranche of the new CDO.

The equity holders in the CDO are supposed to be the ultimate risk-bearers. You can leverage the structure by creating more senior tranches of bonds that would be open to outside investors. You could expand the structure further through a mezzanine layer – which carries less risk than that of the equity tranche but more than that of the senior bonds. You could look at those senior tranches as eurozone bonds.

The big difference between a eurozone CDO and a subprime CDO is the the nature of the backstop. When the eurozone CDO fails, there are no governments that can bail it out because the governments themselves are already the equity holders of the system. This leaves the European Central Bank as the last man standing.

But the whole idea of setting up a eurozone CDO is to avoid this outcome.

If you wanted an ECB-backed solution, you could simply grant a banking licence to the EFSF, which would make it eligible as an official central bank counterparty. I also like George Soros’ idea to focus the eurozone rescue fund solely on bank recapitalisation, in addition to a mechanism that allows eurozone countries to issue short-dated discount bonds at low interest rates.

Both solutions rely heavily on active co-operation by the ECB. Unfortunately, Europe’s central bank may not accept such a role because of the way it interprets its mandate, as described by the Maastricht Treaty and its own statutes.

The real reason why European officials are pursuing the CDO option is to get round this technical obstacle. Remember that one of the main reasons why banks created CDOs in the first place was “regulatory arbitrage”, as it was euphemistically known at the time. In that case, the idea was to circumvent capital adequacy rules. CDOs allowed banks to push risky assets off their balance sheet, which gave more room to make further loans.

In the case of eurobonds, the idea is also to circumvent Article 123 of the European Treaties (which says that the ECB must not monetise debt); the ECB’s governing council; the German Constitutional Court; as well as the Bundestag and other national parliaments. What better instrument than a opaque CDO to get round those inconvenient obstacles of democratic opposition, constitutional law and international treaties.

Do not get me wrong: I am in favour of an enhanced EFSF. The current mechanism is not big enough to protect Italy and Spain, and inject fresh capital into eurozone banks. That would require a lending ceiling three of four times the current size. But we cannot get there through dirty financing tricks that have demonstrably failed in the past. If this CDO were to collapse, the eurozone might face an imminent break-up that could trigger a global financial crash.

If you accept the political and legal constraints as a given, there are no easy policy options left. There exist only two categories of solutions to the crisis: a fiscal solution or a monetary one. Politics blocks the first, European law blocks the latter. The CDO is an alluring idea from the perspective of a technocrat who has to come up with something that satisfies current political preferences and that respects perceived or actual legal constraints.

On the surface, it appears as if a CDO was a third category in itself. But that is not the case because it ultimately dumps the burden on the ECB, just as the subprime mortgage CDOs became a liability for governments.

As I have argued previously, European laws and current political preference are inconsistent with the survival of the eurozone. Something will have to give. A CDO is not a solution to the crisis. It is the last confidence trick in the toolbox of the truly desperate. The eurozone is about to kick the can a final time.

Dexia on brink as France and Belgium work on lifeline

by Dylan Lobo - Citywire.co.uk

French and Belgium officials are working around the clock to provide beleaguered bank Dexia a lifeline.

The Franco-Belgium bank, which narrowly avoided a collapse in the 2008 crisis, continues to face major headwinds due to the freeze in inter-bank lending markets and its high exposure to Greek debt. The bank needs to find away to dispose of another €20 billion of bad debt after managing to dispose of around €80 billion worth of toxic loans since the credit crunch.

Reports suggest ministers from France and Belgium are set to meet to discuss a rescue package for Dexia as the possibility of a Greek default grows by the day. The situation has become even more critical after the Greek government warned it would miss it deficit targets.

The French banking system is close to breaking point due to its relatively large exposure to Greek debt, along with other weak members of the eurozone. On 14 September Moody's downgrade Credit Agricole and Societe Generale, while BNP Paribas was put on review for a potential downgrade.

Dexia put on downgrade watch

by Stanley Pignal - FT

Dexia, the Franco-Belgian banking group, on Monday was put on a negative downgrade watch by Moody’s, which cited concerns about a further deterioration in its liquidity position.

The three main operating entities of the Brussels-based group are being targeted for a possible re-rating, which would come on top of a downgrade in early July. Shares in Dexia dropped 9 per cent in morning trading on the news.

Moody’s said “worsening funding conditions in the market” for banks triggered its new stance and reiterated its July concern. “In Moody’s view, Dexia has experienced further tightening in its access to market funding – even to short-term unsecured funding – since the most recent rating action on 7 July,” it said.

Dexia is majority owned by the French, Belgian and Luxembourg governments and state-led bodies such as the Caisse des Dépôts et Consignations, the French sovereign wealth fund. It has traditionally been the biggest operator in the funding of French municipalities, but also runs sizeable retail networks in Belgium and Turkey.

The bank said last week it was “continuing to examine strategic options”, amid press reports that it is actively engaged in talks with France’s Banque Postale and the Caisse des Depots to form an alliance which would help secure its funding.

Dexia declined to comment on the reported moves or on Monday’s downgrade. But people close to the group acknowledge that the current financing situation is “strained”, as short-term markets on which it relies for part of its financing have dried up .

The markets situation has caused a slump in the value of French banks, which are also being hurt by their holdings of Greek sovereign debt. In the last three months, Dexia’s shares have fallen 40 per cent to €1.33. BNP Paribas shares have fallen 48 per cent and Société Générale 56 per cent in the same period.

Dexia has ample capital reserves under the Basel II framework, and passed the recent stress tests with a core tier one ratio of 10.4 per cent. But it is short of tangible equity, another measure of capital favoured by analysts, with only about €5bn left.

Dexia was one of the first European banks to be bailed out in 2008 due to its unorthodox funding strategy, which involved making long-term loans to municipalities funded by short-term borrowings on the financial markets. The same strategy laid low Britain’s Northern Rock, a major mortgage lender.

“The negative [Moody’s] review comes at a time when Dexia is still facing challenges on how to fund its operations. These are to some extent felt by all banks, but Dexia is more exposed because it still has significant short-term financing needs,” says Matthias De Wit, analyst at Petercam, a brokerage.

Dexia’s management, including Jean-Luc Dehaene, a former Belgian prime minister who acts as Chairman, and chief executive Pierre Mariani, a former top aide to French president Nicolas Sarkozy, have the job of de-risking the bank, even at the cost of sacrificing short-term profitability. The bank’s actions are also constrained by the European Commission, which as an antitrust watchdog has imposed strict operating conditions on Dexia.

Banking crisis set to trigger new credit crunch

by Harry Wilson - Telegraph

The global financial system is on the edge of a new credit crunch as the cost of insuring the bonds of banks across the world hits new highs, analysts have said.

Credit default swaps on lenders as far afield as China and Australia, countries that until recently seemed immune to the chaos, have doubled in the last two months to levels not seen since the financial crisis.

In Europe, French and Belgian government officials are due to meet on Monday to discuss the crisis enveloping Dexia as speculation mounts about a possible break-up of the Franco-Belgian lender. Last week, the cost of insuring Dexia bonds hit an all-time high of 900 basis points, nearly double the level just two months ago, meaning the annual cost to insure €10m (£8.59m) of the bonds is £900,000.

"The money ran out in June and what you are seeing now is the beginning of a new credit crunch, except this time it will be truly global, not Western," said one senior London-based credit analyst. Dexia, along with other European lenders, has been hard hit by the closure of the interbank lending markets and the continuing unwillingness of investors to buy the bonds of eurozone banks. "Nothing is really working at the moment. None of the markets are functioning. Until Greece defaults it's hard to see any resolution," said one senior London-based credit analyst.

In China the publicly quoted cost of insuring the bonds of its three lenders for whom prices are available all closed on Friday at the highest levels in more than two years. Credit default swaps on Bank of China bonds have more than doubled since the beginning of August and hit 316.53 basis points at the end of last week, their highest level since March 2009, while the lender's shares hit a 12-month low.

"The worries on China's banks are around the slowdown in growth, however, the symptoms are the same as those we are seeing in Europe," said Simon Adamson, a banks analyst at CreditSights.

A report published last week by CreditSights drew attention to the growing problems of the Chinese banking sector, with some estimates putting the proportion of the lenders' loan books that are non-performing at more than 40pc.

Australian banks, which have been major users of wholesale funding markets, are among those getting caught in the new crunch. Credit default swaps on the bonds of National Australia Bank and Australia and New Zealand Banking Group are not far off double the level they were just two months ago and last week reached 12-month highs.

Markets remain unconvinced that European politicians are capable of dealing with the region's problems. Greece was yesterday reported to have missed the deficit cutting target set for it by the EU and the IMF as part of the terms of its bail-out. According to Reuters, the Greek budget deficit will reach 8.5pc of GDP this year, missing a target 7.6pc.

An emergency meeting of eurozone finance ministers will today meet in Luxembourg to discuss the progress of Greek reforms that are necessary to secure the next €8bn tranche of bail-out money. Greece is to unveil new austerity measures.

Mad Hatter's tea party that is the eurozone crisis

by Larry Elliott - Guardian

Alice in Wonderland has nothing on the absurd world of Europe's financial policymakers

Curioser and curioser, as Alice said in her adventures in Wonderland. The longer the crisis in the eurozone has gone on, the more it has come to resemble something penned by Lewis Carroll.

Here are just a few of the surreal aspects of the current state of affairs. The answer to a lack of growth in struggling countries such as Greece is austerity of such ferocity that recessions deepen. The solution to a financial crisis caused originally by the over-leveraging of banks and individuals is to turn Europe's bailout fund into a leveraged €2tn hedge fund.

Meanwhile, many of the politicians in Britain who battled long and hard to keep the pound – George Osborne and Ed Balls to name but two – are now born-again evangelists for full fiscal union. How to make sense of all this? It's hard, but as the king says as he presides over the court in Alice in Wonderland: "Begin at the beginning and go on till you come to the end: then stop."

Monetary union was born out of two developments: the idea that there should be ever closer union in Europe and the breakup of the postwar fixed exchange rate system in the early 1970s. The idea was that member states would pool their monetary sovereignty to form one currency that would have one interest rate set by one central bank. Architects of the grand design argued there would be multiple benefits from the new arrangements: Europe would grow closer together, it would become more stable and it would grow faster.

To those who insisted that a one-size-fits-all monetary policy would never work, and that slower, asymmetric growth would lead to the build-up of economic and financial pressures, the response from those banging the drum for the single currency was classic Carroll: "No, no! Sentence first – verdict afterwards."

Predictably, the stresses and strains inherent in a monetary arrangement that involved yoking together countries as diverse (not just economically but culturally) as Germany and Greece, Portugal and Finland, Austria and Spain quickly manifested themselves. The weaker countries on the periphery saw their costs of production rise more rapidly than those at the core, and gradually became less competitive as a result. Although Europe as a whole saw its trade balance remain close to zero, Germany ran a hefty trade surplus at the expense of Italy, Spain and Greece.

Speculative orgy

Just as China recycled its trade surplus into the global economy through the purchase of US treasury bonds, so Germany's surplus headed south to fuel property bubbles in Spain and to finance excessive borrowing by Greece. The actions of China and Germany kept the speculative orgy going for a while, but only by making the eventual hangover worse.

In the days before monetary union, a country that had seen its competitiveness eroded had an easy, if not painless, remedy. It would devalue its currency, making its exports cheaper and its imports dearer. Inflation would go up and structural weaknesses would be ignored, but it was a way of rubbing along. Inside the single currency, there is only one way a country such as Greece can compete with Germany and that is to lower the cost of the goods and services it produces.

That means lower wages, smaller pensions and deep cuts in public spending. And not just for one or two years: the adjustment process within monetary union involves decades of austerity. For the Greeks and the Italians, the message is jam tomorrow and jam yesterday but never jam today.

The climax of Alice in Wonderland is the courtroom scene in which the issue is "Who stole the tarts?" In the case of the eurozone, the easy answer is that it is Greece, which failed to play by the rules, borrowing too much and cooking the books so that the rest of the members of the single currency club were ignorant of the dire state of the Hellenic public finances.

In fact, the real culprit is Germany, which has failed to appreciate that for monetary union to work, the big creditor nations have a responsibility to help the debtor nations by expanding domestic demand. The German political class appears to believe both that every country in the euro area can be as competitive as Germany and that Germany, in those circumstances, will continue to run a massive trade surplus. That's a logical absurdity the Reverend Dodgson would certainly have appreciated.

To make matters even more deliciously weird, Berlin now faces a dilemma. The crisis in the euro area has been allowed to fester for the best part of two years, allowing the contagion to spread from Greece to other peripheral countries. As a result, the cost of cleaning up the mess has grown enormously. The first bailout for Greece in May 2010 was just over €100bn.

By the time of the emergency eurozone summit in July 2011, it was deemed necessary to expand the European financial stability facility to create a €440bn fighting fund. Two months or so later, the perception is that Europe will need to have €2tn, perhaps even €3tn, to face down the financial markets.

It is unclear, as yet, how European policymakers intend to turn one euro into five, but it seems to involve setting up a special purpose vehicle backed by Germany and France. At its core will be the EFSF, which will be underpinned by financial guarantees from Berlin and Paris. The EFSF will not be increased from €440bn, but will be used as collateral to expand the scale of bond purchases to support the weaker states.

Even assuming the rating agencies are happy with this (and they may not be), Germany and France would be putting their creditworthiness at risk. Put simply, they would be betting the farm on a highly leveraged special purpose vehicle. Deja vu, anyone?

Yet the alternative does not look all that attractive either. Germany could, in theory, declare that it was no longer prepared to write the bailout cheques for the rest of Europe. It could start printing some lovely new deutschmarks or perhaps start exploratory talks with the Austrians, Finns and Dutch about a hardcore euro made up of half a dozen broadly convergent economies.

But even assuming this could be achieved without plunging not just Europe but the rest of the global economy into a second Great Depression (and it probably could not), the upshot would be that German banks would face potentially ruinous losses on a wave of sovereign debt defaults, while German exporters would be priced out of overseas markets because the new DM would appreciate sharply on the foreign exchanges.

Up until now, policymakers have solved this dilemma by refusing to admit that it exists. The assumption has been that the events of the recent past have all been a bad dream from which Europe will wake up. Only recently has it been recognised that the single currency really is plunging down a rabbit hole and is going to hit the ground with an almighty bump.

And to those who say that out of the wreckage will emerge a full-blown fiscal union that Britain stands apart from at its peril, the adventures of Alice provide the perfect riposte. "If everybody minded their own business," said the Duchess, "the world would go round a good deal faster than it does."

Is Germany's Finance Minister Going Rogue?

by Laura Gitschier, Peter Müller, Christian Reiermann and Michael Sauga - Spiegel

He used to be regarded as Germany's safest pair of hands when it comes to the euro crisis. Now, criticism of Finance Minister Wolfgang Schäuble is growing within the government parties. Some believe that Schäuble wants to exploit the crisis to push through his vision of a United States of Europe.

A pall of silence fell over the German parliament as Finance Minister Wolfgang Schäuble went up to the lectern last Thursday. The debate over the expansion of the euro backstop fund, the European Financial Stability Facility (EFSF), had already been going on for over an hour. Previous speakers addressing the Bundestag had tried their hand at a number of different roles. Schäuble's predecessor in office, Peer Steinbrück of the left-leaning Social Democrats (SPD), had tried to present himself as a European statesman, whereas Rainer Brüderle, the parliamentary floor leader for the business-friendly Free Democratic Party (FDP), had vehemently attacked the opposition.

Now, it was the turn of Schäuble, a member of the center-right Christian Democratic Union (CDU). He feigned the honest broker who tries to mediate between the parliament's legitimate demand to have a say in such important matters and the exigencies of international political crises. "No one here sees this as an easy decision," he said. The question at hand, he continued, is whether politicians are capable of "controlling these developments."

The government, it seems, is certainly able to exercise control, at least when it comes to maintaining discipline within its own ranks. German Chancellor Angela Merkel and Peter Altmaier, the conservatives' parliamentary secretary, exchanged congratulatory text messages after winning the key Bundestag vote on the euro bailout fund: "Our efforts paid off."

Two things became clear at the end of last week -- a week that many pundits had prematurely predicted would spell the end of the center-right coalition of the CDU, its Bavarian sister party the Christian Social Union and the FDP. First, the government can rely on its own parliamentary majority to push through euro bailout legislation -- at least for the time being. Second, Merkel's finance minister, of all people, has sown doubt about the government's crisis management. In the days running up to the vote, Schäuble needlessly fueled a debate over expanding the euro backstop fund, and his comments sparked renewed tensions within the coalition.

Keeping His Cards Close to His Chest

FDP parliamentarians have long been convinced that the finance minister is not playing with an open hand, and that he would prefer to force them out of the coalition. But there has also been an increasing amount of discontent over Schäuble among the ranks of the CDU/CSU parliamentary group. Quite a number of his fellow conservatives accuse him of undermining their rights as parliamentarians and forging agreements on a European level that he largely keeps under wraps at home. The CSU even suspects that the finance minister is paving the way for a European super-state, something that the Bavarians strongly oppose.

This criticism is directed at one of the last political heavyweights in Merkel's cabinet. For months now, Schäuble has topped the opinion polls as one of Germany's most popular ministers. No one else on the nationwide political scene enjoys such high regard, even across party lines. The Germans believe that if anyone can steer the country through the perils of the euro crisis, it's Schäuble, with his extensive experience in political maneuvering. The veteran party and parliamentary group leader stands at the twilight of his career and doesn't have to prove anything to anyone anymore -- and is not aspiring to any position.

This makes him a formidable figure, but it also feeds his longstanding tendency toward arrogance and his penchant for political intrigues. Many conservative parliamentarians, regardless of their position on the common currency, feel as if they are being treated with contempt. His statements made during the euro crisis have rarely been unequivocal; he always leaves himself a way out. Not only does this confuse his political friends and foes, it also flusters the financial world, with its propensity for panic.

Many German politicians are also insinuating that he has a hidden agenda. They fear that one of the last fully committed supporters of the European project is taking advantage of the crisis to advance his dream of a United States of Europe -- at almost any price. Even the chancellor is sometimes annoyed by the finance minister's moves.

Pithy German Wisdom

Schäuble's antics last week were a perfect example of his modus operandi. It began with business as usual. At the fall meeting of the International Monetary Fund (IMF) and the World Bank in Washington, the finance minister used quaint German phrases to broach the topic of the crisis in the euro zone. Referring to the fact that every country in the monetary zone is first and foremost responsible for the soundness of its own finances, he recited a quotation by Goethe: "Let everyone sweep in front of his own door, and the whole world will be clean."

Schäuble finds himself irresistible at such moments. He is not bothered by the fact that foreigners and representatives of the international media who he is addressing have no idea what to make of such Teutonic pearls of wisdom.

To make matters worse, Schäuble often doesn't even adhere to his own admonishing axioms. "Silence is golden," he decreed in Washington, a reference to the need to avoid panicking markets with loose talk. But then he heedlessly allowed himself to be drawn into a dangerous debate over whether the EFSF could get a banking license and leverage its assets to borrow even more money from the European Central Bank (ECB).

Most of his German predecessors in office would have rejected such notions with indignation and referred to Germany's traumatic experiences during the 20th century, when governments printed money to finance public expenditure, causing the value of the currency to plummet.

Merkel Intervenes

Not once, however, did Schäuble clearly reject the proposals, which had been spearheaded by his American counterpart, US Treasury Secretary Timothy Geithner. Instead, he talked about alternatives to a banking license, which would make it possible to achieve similar leverage effects. Schäuble did not exactly say just what these alternatives might be, but he did mention that Berlin is considering bringing forward the launch of the European Stability Mechanism (ESM), the permanent bailout fund for the euro zone, from 2013 to 2012.

In addition to being imprudent, Schäuble's comments showed bad timing. Ironically, during the very week in which the coalition was struggling for a parliamentary majority to extend the reach of the euro backstop fund, Schäuble was publicly contemplating yet another reform of the initiative.

German Vice Chancellor Philipp Rösler, the leader of the FDP, is appalled. "Granting a banking license to the European bailout fund would be the wrong approach," he says, adding that such a step could be interpreted as a sign "that the finance minister has been given a license to print money." It took an intervention by the chancellor herself to clear up the matter. She informed Schäuble that there would be no solution that involved integrating the ECB.

Concealing His True Intentions

The chancellor and her supporters had spent weeks ensuring that the center-right coalition government could muster an outright majority in favor of the euro backstop fund. In exchange for their votes, parliamentarians were offered significantly greater oversight of EFSF operations. Everything was going well -- until the finance minister made his botched appearance in Washington.

Just how much is at stake for the chancellor was made clear by a comment that she made, almost in passing, as she ended her speech to the conservatives' parliamentary group last Tuesday. Merkel told them that she didn't want to be dependent upon the votes of the two main opposition parties, the SPD and the Greens, who had both pledged to support the bill. Then, she made a direct appeal to her parliamentarians, saying she couldn't allow that to happen because "I still have far too many plans for us." In other words: She wants to continue to govern with the current coalition.

However, there has long been much speculation within the ranks of the coalition over whether the finance minister shares that goal. Schäuble has repeatedly indicated his support for a so-called grand coalition with the SPD, similar to the one that ruled German between 2005 and 2009. His ongoing tendency toward secrecy has caused much consternation within the coalition. Recently, for instance, the finance minister only shared his first draft for the new EFSF agreement with the parliamentary floor leaders of the different parties and a number of interested politicians.

By contrast, Schäuble didn't say a word about it to the CDU/CSU parliamentary group. A senior member of the parliamentary group caustically commented that Gregor Gysi, the floor leader of the far-left Left Party, "knew about it before Schäuble's own colleagues in the CDU."

Once again, the coalition parliamentarians had the feeling that they were the last ones to be informed by the minister. And, once again, they discovered that Schäuble was using a torrent of words and statements in an attempt to conceal what he is really planning and thinking.

Bag of Tricks

Schäuble's political style is also characterized by a good deal of posturing. No other politician in Berlin can so convincingly play the innocent bystander, and no one is better than the finance minister at deflecting attention from his own mistakes.

Last Thursday, as the entire country was talking about the idea of leveraging the bailout fund, he profusely vented his indignation in front of the FDP parliamentary group about others who had supposedly broached this dangerous issue. He told them that he was "exceedingly" annoyed that Olli Rehn, the European commissioner for economic and monetary affairs, was making "such proposals." Then he spelled out his position: "We are not increasing the scope of the fund; we are merely safeguarding the €440 billion." This still leaves Germany with a liability risk of €211 billion, he said. "I am not committing to anything beyond that, just so you don't later accuse me of telling you something that isn't true."

That certainly sounded convincing, but Schäuble had merely demonstrated another tactic from his bag of tricks as a seasoned politician: the denial that isn't actually a denial. At issue here was not whether the fund would be expanded even further, but whether there were plans to pursue clever leveraging with the volume available. "On Thursday, the parliamentarians were voting on a black box," says CDU financial expert Manfred Kolbe, who voted against the EFSF ratification.

Indeed, it is now already clear that, along with the planned guarantees for €440 billion, a considerably larger sum of money will also be mobilized among banks and insurance companies to support, if necessary, Italy and Spain, should Greek Prime Minister Georgios Papandreou be forced to declare his country bankrupt.

Increasing Risk

It would work like this: The EFSF fund would promise investors that if they purchase Italian or Spanish government bonds it would cover, say, up to 20 percent of their loses. This would render the bonds from these countries more attractive to investors, making them more willing to make fresh money available.

The effective financing volume of the bailout fund would thus increase fivefold. If the fund were to cover 25 percent of losses, the firepower of the EFSF would be ramped up by a factor of four. What makes this solution so appealing is that, according to government lawyers, the entire process could take place within the legal framework of the euro backstop fund, and its regulations would not have to be amended and passed by the Bundestag again. The approval of the parliament's budget committee would suffice. Nevertheless, this approach would further increase the government's credit risks.