"Looking up Market Street from near Ferry", San Francisco in the aftermath of the earthquake and fire

Stoneleigh: Our most consistent theme here at The Automatic Earth has been the developing deflationary environment and the knock-on effects that will follow as a result. Now that the rally from March 2009 appears to be well and truly over, it is time to revisit aspects of the bigger picture, in order for people to prepare for a full-blown liquidity crunch. October 2007-March 2009 was merely a taster.

As we have explained before, inflation and deflation are monetary phenomena - respectively an increase and decrease in the supply of money plus credit relative to available goods and services - and are major drivers of price movements. They are not the only price drivers, to be sure, but they are usually the most significant. People generally focus on nominal prices, when understanding price drivers is far more important. A focus merely on nominal price also obscures what is happening to affordability - the comparison between price and purchasing power.

We have lived through some 30 years of inflationary times, since the financial liberalization of the early 1980s under Reagan and Thatcher initiated the era of globalization. Money freed from capital controls was free to look for opportunities worldwide, and the resulting global economic boom greatly increased trade, resource consumption, financial interconnectedness and the multiplier effect for monetary expansion.

The increased purchasing power that resulted, largely for the better off, found its way into asset markets around the world, allowing people to bid up prices. This created a psychological 'wealth effect', which spawned an orgy of consumption through borrowing against rising nominal assets values. This in turn led to greater monetary expansion, since money is lent into existence. Fractional reserve banking, securitization, the enormous expansion of the shadow banking system and many other factors acted as engines of monetary expansion.

This spiral of positive feedback started slowly, but gradually morphed into a global mania of epic proportions. Caution was thrown to the wind, debt expanded exponentially, risk multiplied, wealth concentration increased with higher returns to capital and consumption became almost frenetic where increasing purchasing power supported it. At the same time, rising consumer prices put increasing pressure on the less privileged, who were forced to compete for basic necessities becoming ever more expensive. As we have seen in a number of places, this has been a major ingredient in the development of social unrest. High prices, and fear of both higher prices and actual shortages, can be socially explosive.

Rising prices are not themselves inflation, as we have repeatedly explained, but are the result of it. Credit expansions create excess claims to underlying real wealth through the creation of artificial, or virtual, value. They also bring demand forward, increasing pressure on resources for the duration of the expansion period. Extrapolating consumption trends forwards linearly leads to fear of shortages, which encourages market participants to bid up prices speculatively.

However, being based on Ponzi dynamics, credit expansions and speculative manias are naturally self-limiting. Credit expansions proceed until the debt they generate can no longer be serviced, and there are no more willing borrowers and lenders to continue lending money into existence. Speculative manias continue until the greatest fool has committed himself to the exhausted trend, and no one remains to push prices up further.

As an expansion develops, one can generally expect increasing upward pressure on commodity prices, thanks to both demand stimulation and latterly the perception that prices can only continue to increase. The resulting crescendo of fear - of impending shortages - is accompanied by the parabolic price rise typical of speculative bubbles, as momentum chasing creates a self-fulfilling prophecy. At the point where almost everyone with the capacity to do so has jumped on the bandwagon, and all agree that the upward trend is set in stone, a trend change is typically imminent.

We find ourselves still near the peak of the largest credit bubble in history. As faith in many of the more spurious 'asset' classes devised by 'financial innovation' has been shaken, faith in the ever increasing value of commodities has strengthened. However, commodities are not immune to the effects of a shift from credit expansion to credit contraction, despite justifications for endless price rises, such as apparently bottomless demand from China and the other BRIC countries.

Every bubble is accompanied by the story that it is different this time, that this time prices are justified by fundamentals which can only propel prices ever upwards. It is never different this time, no matter what rationalizations exist for speculative fervour. BRIC demand only appears to be insatiable if we make our predictions solely by extrapolating past trends, but that approach leaves us blind to trend changes and therefore vulnerable to running off a cliff. Insatiable demand results from seemingly endless cheap credit, given that demand is not what one wants, but what one can pay for. When credit collapses, so will demand, and with it the justification for higher prices.

While credit expansion (inflation) is a powerful driver of increasing prices, credit contraction (deflation) is a far more powerful driver of decreasing prices. Credit, having no substance, is subject to abrupt fear-driven disappearance. Confidence and liquidity are synonymous, and confidence is once again evaporating quickly, as it did in phase one of the credit crunch (October 2007-March 2009). As contraction picks up momentum, the loss of credit will rapidly lead to liquidity crunch, drastically undermining price support for almost everything. With purchasing power in sharp retreat, however, lower prices will not lead to greater affordability. Purchasing power typically falls faster than price under such circumstances, so that almost everything becomes less affordable even as prices fall.

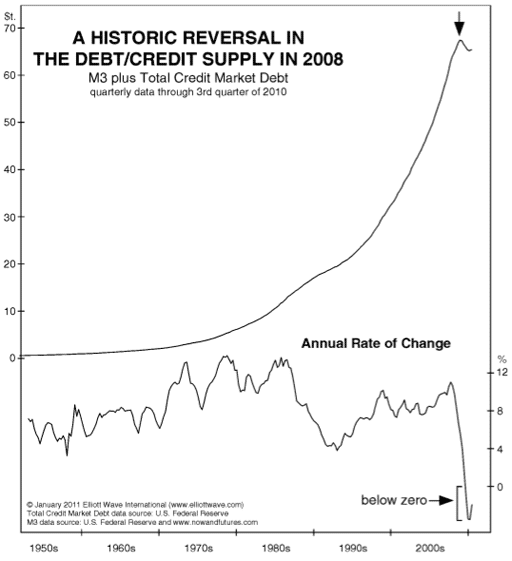

Credit expansion reversed in 2008, and this is deflation by definition. Despite the talked-up attempts to monetize debt through quantitative easing - a deliberate attempt to stoke inflation fears in order to counteract the psychology of deflation - money plus credit has been in net contraction. Talk of monetary growth based on only the money fraction misses the elephant in the room, since the vast majority of the effective money supply is credit, and the tightening of credit is by far the dominant factor.

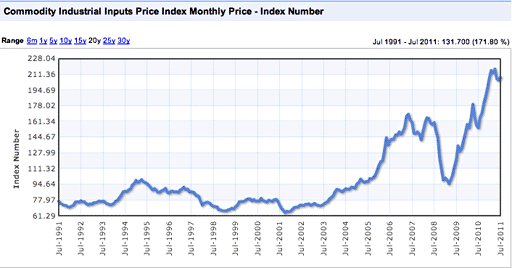

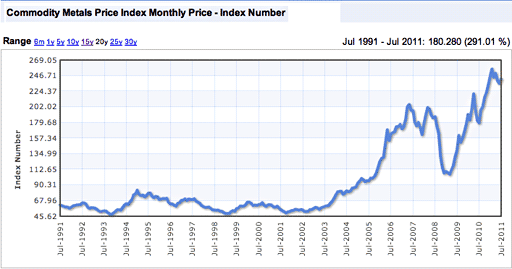

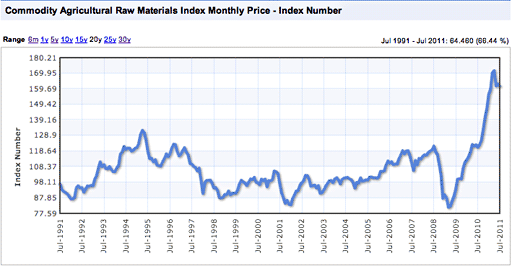

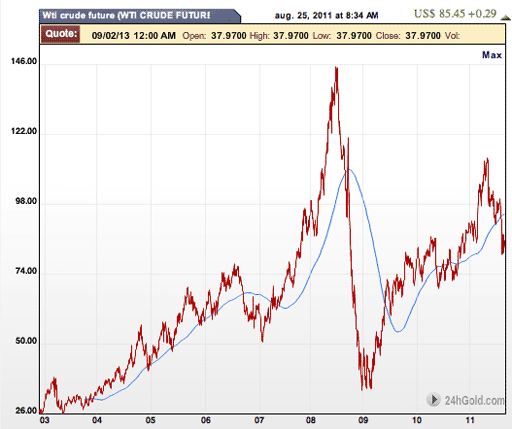

As one can see from the graph, credit reversal had not occurred for decades until 2008. Now that it has done so, we can expect significant consequences to follow. There is a constellation of trends that had been correlated with the ebb and flow of liquidity, for instance increasing equities and commodities and a falling dollar. The end of the recent large counter-trend rally has already seen equities and commodities begin to fall, and a reversal in the fortunes of the dollar is very likely in the not too distant future. A look at long term charts of the various different commodities demonstrate both the parabolic run up in prices since 2009, and the beginnings of price retreat. This is likely to be a top that lasts for quite some time in a persistent deflationary environment, at least for the less essential factors.

Food and energy price falls come as a surprise to many, given that both are necessities in a very heavily populated world. Energy is the master resource, and net energy analysis demonstrates that supply can no longer increase meaningfully, hence the commonly held opinion that prices can only move in one direction. However, that opinion also held sway in 2008 during a previous speculative episode, and a closer look at oil prices reveals that that period ended in typical bubble fashion, with a sharp fall following the parabolic rise.

At the time, we were warning that exactly this scenario would unfold, which was an unpopular opinion. The secondary bubble formed in the price run up from 2009 is destined to end the same way, with a fall to a lower level than the 2009 bottom. Supply problems further down the line will ensure that the bottom is strictly temporary, and that future price spikes are in the cards, but that is tomorrow's issue rather than today's.

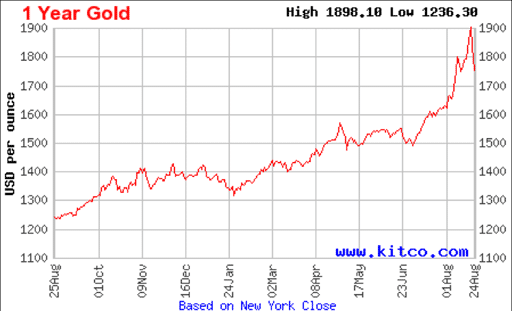

Of all the commodity bubbles, it is the end of the explosive rise in gold that is set to surprise the largest number of people. Very few expect it to follow silver's lead, but that is exactly what we are suggesting.

Gold has been increasingly considered to be the ultimate safe haven. The certainty has been so great that prices rose by hundreds of dollars an ounce in a blow-off top over a mere two months. The speculative reversal currently underway should be rapid and devastating for the True Believers in gold's ability to defy gravity eternally. Expect to hear all about the enormous Ponzi scheme in paper gold, and a lot more about plated tungsten masquerading as gold. It doesn't even matter whether or not that rumour is true. What matters is whether or not people believe it, and how it could feed into a spiral of fear as prices fall.

Central banks are buying gold, which some consider to be a major vote of confidence, and therefore bullish for gold prices. However, it is instructive to look at the previous behaviour of central banks in relation to gold prices. When gold hit its low point eleven years ago, after a long and drawn out decline, central bankers were selling, in an atmosphere where gold was dismissed as a mere industrial metal of little interest, or even as a 'barbarous relic'.

Selling by central banks, which are always one of the last parties to act on developing received wisdom, was actually a very strong contrarian signal that gold was bottoming. They would not have been selling if they had anticipated a major price run up, but central banks are reactive rather than proactive, and often suffer from considerable inertia. As a result they tend to be overtaken by events. Regarding them as omnipotent directors and acting accordingly is therefore very dangerous.

Now we are seeing the opposite scenario. After eleven years of increasingly sharp rise, central banks are finally buying, and they are doing so at a time when the received wisdom is that gold will continue to reach for the sky. Once again, central banks are issuing a strong contrarian signal, this time in the opposite direction. While commentators opine that central banks will hold their gold even if they develop an urgent need for cash, this is highly unlikely. In a deflationary environment, it is cash that is scarce, and cash that everyone, including central bankers, will be chasing. Selling gold to raise cash may well not be a matter of choice.

Typically a speculative bubble is followed by the reversal of speculation causing prices to fall, and then by falling demand, which undermines prices further. As the bubble unwinds, people begin to jump on a new bandwagon in the opposite direction, chasing momentum as always. The need to access cash by selling whatever can be sold (rather than what one might like to sell), and the on-going collapse of the effective money supply as credit tightens mercilessly, will also factor into the developing vicious circle.

Gold has been considered money for thousands of years, and will hold its value over the long term. However, this does not preclude a huge downward move in the shorter term, and for those forced to sell early, there is no longer term perspective. Spot prices will fall, but those with no bargaining power will get much less than the spot price if they are forced to sell into what is likely to be the ultimate buyers market during the next few years. They will never be able to buy back into the market, and would generally have been better off holding the cash that will appreciate in value for the few years of the credit collapse. Only those who can genuinely hold gold for the duration of the deleveraging, without having to rely on the value it represents in the meantime, will really be able to use it as a store of value.

We stand on the verge of a precipice. The effects of the first real liquidity crunch for decades will be profound. We are going to see prices fall across the board, but far fewer will be able to afford goods or assets at those lower prices than can currently afford them at today's lofty levels. The social effects of this will be enormous, and will spread to many more countries. The collapse of our credit pyramid will be the driving factor and it will sweep all before it like a hurricane for at least the next several years. Beware.

How Long Can the ECB Prop Up Europe’s Sick Banks?

by Simon Kennedy and Gavin Finch - BusinessWeek

The region’s banks may have so much bad debt they won’t even lend to each other

Four years to the month since the global credit crisis began, the European Central Bank has emerged as the lender of first resort to the Continent’s broken banks. With the bond market shut off to all but the strongest lenders, the ECB’s unlimited loans are keeping the most afflicted banks in Greece, Portugal, Italy, and Spain afloat. "Banks are becoming more nervous about being exposed to other banks as they hoard liquidity and become more suspicious of other banks’ balance sheets," Guillaume Tiberghien, an analyst at Exane BNP Paribas, wrote in a note to clients on Aug. 19.

On that date, banks deposited €105.9 billion ($152 billion) with the ECB overnight, almost three times this year’s average, rather than lend the money to other banks. They are also stockpiling dollars and hoarding cash in safe havens such as Swiss francs. "I’m not sleeping at night," says Charles Wyplosz, director of the Geneva-based International Center for Money and Banking Studies. "We have moved into a new phase of crisis."

Investors are concerned, too. The price of European bank stocks sank 22 percent between Aug. 1 and Aug. 22, led by Royal Bank of Scotland (down 45 percent) and France’s Société Générale (down 39 percent). The extra yield investors demand to buy bank bonds instead of benchmark government debt surged to 2.98 percentage points on Aug. 19, the highest since July 2009, data compiled by Bank of America Merrill Lynch show.

Despite the ECB’s best efforts, some of Europe’s banks may be inching toward insolvency. The cost of insuring the bonds of 25 European banks and insurers set a record high on Aug. 24 of 257 basis points, higher than the 149 basis-point spike when Lehman Brothers collapsed in the fall of 2008, according to the Markit iTraxx Financial Index of credit default swaps. The banks aren’t required to mark down most of their holdings of government debt to market prices. If they did, some would be forced to default or seek a bailout.

Morgan Stanley (MS) estimates that Europe’s banks need to raise €80 billion by yearend. Their ability to raise capital has been sharply curbed by investor fears. Banks in the region hold €98.2 billion of Greek sovereign debt, €317 billion of Italian government debt, and about €280 billion of Spanish bonds, according to European Banking Authority data.

The Federal Reserve, which provided as much as $1.2 trillion of loans to banks in December 2008, wound down most of its emergency programs by early 2010. One of the few exceptions is the central bank liquidity swap lines that provide dollars to the ECB and other central banks, so they can auction off the dollars to banks in their own jurisdictions.

In contrast, the ECB and its president, Jean-Claude Trichet, are still in the bank-rescuing business. "The central bank is the only clearer left to settle funds between banks," says Christoph Rieger, head of fixed-income strategy at Commerzbank in Frankfurt. After increasing its benchmark rate twice this year to counter inflation, the ECB in August provided relief for banks by buying Italian and Spanish bonds for the first time, lending unlimited funds for six months and even providing one unnamed bank with badly needed dollars.

The ECB is maintaining a role it began in August 2007 when it injected cash into markets after they froze. The ECB’s balance sheet is now 73 percent bigger than in August 2007, and its latest round of bond buying has opened it to accusations that by rescuing profligate nations it’s breaking a rule of the euro’s founding treaty and undermining its credibility.

The central bank is acting in part because governments have yet to ratify a plan to extend the scope of a €440 billion rescue facility so it can buy sovereign bonds on the open market, which would allow governments to inject capital into the banks. Although the euro zone member governments are supposed to approve the new funding by fall, no one can say for sure.

The funding difficulties of Europe’s banks is one reason cited by Morgan Stanley economists on Aug. 17 for cutting their forecast for euro-area growth to 0.5 percent next year, less than half the 1.2 percent previously anticipated. Europe’s consumers and companies are more reliant on banks for funding than their U.S. counterparts, says Tobias Blattner, a former ECB economist now at Daiwa Capital Markets Europe in London.

Lena Komileva, Group of 10 strategy head at Brown Brothers Harriman in London, says the ECB may have no option but to extend the backstop role it is playing. Refusal to do so would risk a European bank default by the end of the year, she says: "Markets are back in uncharted territory. The crisis is a whole new story now."

The bottom line: Some European banks hold almost half a trillion euros in questionable government bonds. They’re relying on ECB funding to stay in business.

US funds show true state of eurozone banks

by Gillian Tett - FT

In any murder mystery film, it pays to watch the boring grey man (or woman) in the corner; quiet, unobtrusive characters can be deadly.

So, too, in finance. Four years ago, the giant US money market funds seemed some of the dullest actors in the global financial scene. But in 2007, they quietly helped to spark the crisis in the mortgage-backed securities world, when they silently stopped rolling over bonds. Then, in 2008, they furtively wielded the knife again, pulling funding from some American banks and the "repo" – repurchase – markets.

Now, their shadow looms again. As my colleagues Dan McCrum, Telis Demos and Jennifer Hughes have reported, in recent weeks these funds have been quietly backing away from European banks, either refusing to roll over loans, or slashing the maturities of the funds they provide. Fitch, for example, recently calculated that the largest US money market funds cut their exposure in absolute terms by $30bn in July, even before the latest turmoil.

Separately, bankers estimate that Italian banks lost the equivalent of €40bn-worth of money market funding in July. And while money market funds are still lending to French banks, the duration of deals has shrivelled dramatically, from several months to just a few weeks (at most). This matters, since French banks rely on money markets for about €200bn of funding.

Now, the good news is that these raw numbers are small compared to the total volume of money that eurozone banks raise in the wholesale and interbank markets, which is around €8,000bn. Better still, the European Central Bank has stepped into the gap to replace those vanishing funds. That has kept the system running, even as funding costs for eurozone banks have exploded to a level which are "massively prohibitive" – and thus unsustainable – for most banks, as Suki Mann, analyst at Société Générale says.

But it is worth watching what those money market funds do next. For one thing, their antics tend to have a powerful impact on market psychology, particularly given folk market memories of 2008. Secondly, this quiet exodus has reminded US and European investors alike of something that policymakers have hitherto tended to downplay: namely the rather surprising degree to which eurozone banks depend on short term financing.

Morgan Stanley, for example, calculates that of the €8,000bn funding that is currently in place for the largest 91 eurozone banks, some 58 per cent needs to be rolled over in the next two years. More startling still, some 47 per cent of this funding is less than a year in duration. Much of that is in euros.

However, as the saga of the money market funds shows, eurozone banks have been raising short-term dollar funds too, either to finance their portfolios of dollar assets, or to provide a cheap form of funding (which is then swapped back into euros.) The scale of this reliance is – thankfully – not nearly as large as it was in, say, 2007; back then eurozone banks had a vast network of dollar-funded mortgage vehicles, creating a funding mismatch that was about $800bn, according to the Bank for International Settlements. Nevertheless, some element of this mismatch remains; hence the current crunch.

Is there any solution? In the long term, some eurozone banks probably need to rethink some of their funding profile. In the short term, however, Huw van Steenis, an analyst at Morgan Stanley, has recently been promoting another interesting idea: eurozone authorities should offer joint guarantees for debt issued by banks, as a form of "circuit breaker" to counteract panic.

After all, the argument goes, the US offered such guarantees during its banking crisis, with considerable success. So did the UK. And if the eurozone authorities were to repeat this trick across the region – say by using funding from the European financial stability facility, supplemented with a fee recouped from banks – it might well tempt money market funds (and others) back. After all most US money market funds are frantic to find somewhere – anywhere – safe to stash their cash, other than US Treasuries.

Will this happen? Don’t bet on it soon. After all, the official line from the eurozone policy world is that nothing is really wrong with the eurozone banks; thus they do not want to introduce crisis measures that echo 2008. Nor do they want to start arguing about how to price or fund any such guarantees, since that might force them to state which banks – and national banking systems – look risky.

But if the unease stalking the eurozone banking system does not dissipate soon, the concept of such "circuit breakers" should certainly be put on the table. And in the meantime, better keep watching those money market funds like a hawk; if nothing else, they are a powerful litmus test of just how much (or little) "credit" those eurozone banks can still attract on the world stage. In both the Latin and English sense of the word.

Bank job cuts top 60,000

by Harry Wilson - Telegraph

ABN Amro has become the latest bank to announce thousands of staff cuts as the total number of jobs lost in the banking sector in recent months rose above 60,000.

The Dutch bank said it will cut 2,350 staff, or just under 10pc of its workforce, over the next three to four years as part of a wholesale restructuring of its business designed to saved hundreds of millions of euros in costs.

Taking the cuts announced by ABN into account, the total number of banking sector job losses announced in recent months now exceeds 60,000 or roughly 5pc of the industry headcount. ABN said 1,500 jobs would be cut through redundancies and a further 850 through natural attrition, costing the bank €200m (£176m) in restructuring costs, according to its financial results for the first half of the year published today.

Earlier this week, UBS confirmed speculation that it was to cut several thousand jobs, announcing the layoff of 3,500 staff, or which about 300 are expected to come from the bank’s London office. All of Britain’s major banks, with the exception of Standard Chartered, have already cut or are cutting thousands of staff. Barclays has already cut 1,400 staff this year and plans to cut as many as 3,000 more jobs within the next 18 months.

HSBC has announced the cull of about 30,000 staff by the end of 2013, or about one in 10 jobs, as part of its own cost drive, and state-backed lender Royal Bank of Scotland is expected to reduce the workforce in its investment banking division by 2,000 within the next year.

The largest cuts have come as Lloyds Banking Group, which announced 15,000 "role reductions" as part of its strategy review, which will take the total number of jobs lost at the lender since its taxpayer bailout to about 40,000 – roughly equal to the size of the entire workforce of engineering company Rolls Royce.

"When managements resort to headcount reductions, these are a powerful signal that firms think the revenue outlook has weakened beyond just normal volatility," said analysts at Barclays Capital in a note to clients published this month. Nearly all of Europe's major banks have announced year-on-year falls in revenues for the first half of the year as markets have deteriorated.

U.S. Banks Said to Seek Relief on Ratios, FDIC Fees After Rush of Deposits

by Dakin Campbell, Dawn Kopecki and Bradley Keoun - Bloomberg

U.S. regulators have asked some banks to take more deposits from large investors even if it’s unprofitable, and lenders in return are seeking relief on insurance premiums and leverage ratios, according to six people with knowledge of the talks.

Deposits are flooding into the biggest U.S. banks as customers seek shelter from Europe’s debt crisis and falling stock prices. That forces lenders to raise capital for a growing balance sheet and saddles them with the higher deposit insurance payments. With short-term interest rates so low, it’s hard for financial firms to reinvest the new money profitably.

Regulators have asked banks to take the deposits anyway, three people said, with one lender accepting $100 billion. The regulators want lenders to take the deposits because it improves the stability of the financial system, according to one of the people, who said U.S. banks are viewed as places of strength.

Some of the largest ones have talked with regulators about softening rules for ratios that measure capital and assets, according to the people, who declined to be identified because talks are private. At least one asked for a waiver on paying higher premiums to the Federal Deposit Insurance Corp., which is less likely to be granted, one of the people said.

"If the helicopter comes raining money on your bank and it’s only temporarily there, it could be excessively costly and disruptive," said Robert Litan, a vice president of research and policy at the Kansas City, Missouri-based Kauffman Foundation, which promotes entrepreneurial business practices.

Cash Cache

Cash held by domestically chartered U.S. banks, which includes Federal Reserve balances, rose to a record $1.02 trillion earlier this month, up 27 percent from the end of July last year. Deposits held by the 25 largest lenders expanded to $4.69 trillion in the week ended Aug. 10, up 8.5 percent from the end of May. The Fed’s balances advanced to $1.61 trillion as of Aug. 24, from $1.05 trillion a year earlier.

The extra deposits are problematic because they’re subject to withdrawal, so banks have to park the money in low-yielding short-term investments, Litan said. With few other choices available, banks have stashed their excess deposits at the Fed, which means the cash gets counted as assets.

This expands their balance sheets and thus pushes down their leverage ratio, which measures Tier 1 capital divided by adjusted average total assets; the lower the ratio, the weaker the bank, at least in theory. In reality, regulators regard U.S. lenders as relatively strong with sufficient capital cushions, the people said.

Talks With Regulators

Lenders have held discussions with officials at the Fed, FDIC, Office of the Comptroller of the Currency and the Treasury Department, according to four of the people. Spokesmen for the four agencies declined to comment.

Regulators may decide, for example, to ease curbs on deposits swept in from brokerage affiliates as part of any forbearance, said James Chessen, chief economist at the Washington-based American Bankers Association. Under normal circumstances, those deposits could be restricted as part of an enforcement action by regulators, he said.

"You don’t want costly business decisions driven by these temporary flows and regulators are acknowledging that and acknowledging the limited risk," Chessen said in a phone interview. "Unusual situations naturally call for a discussion on both sides," he added in an e-mail.

While the Fed has been paying 0.25 percent interest on deposits placed with the central bank, known as interest on excess reserves, since late 2008, it may not be enough to erase the cost to banks of holding the deposits, said Robert Eisenbeis, a former head of research at the Federal Reserve Bank of Atlanta and now chief monetary economist for Sarasota, Florida-based Cumberland Advisors Inc.

Charging Depositors

At least one firm, Bank of New York Mellon Corp. , tried to recoup some of the costs by charging depositors 13 basis points, or 0.13 percent, for holding unusually high balances.

FDIC insurance fees for large banks typically average more than 0.1 percent, three of the people said. In addition, large banks also may apply an internal capital charge of at least 0.1 percent to such reserves, one bank executive estimated. Lenders likely reached out to regulators "after having watched what Bank of New York did," Litan said. "I’m sure the banks said there must be another way."

If the FDIC agreed to forgive some fees, it would have to give up some of the extra premiums that it’s counting upon to rebuild the Deposit Insurance Fund, which covers customers for $250,000 per account in the event of a failure. That makes the agency unlikely to grant a waiver, one of the people said, adding that the existence of the insurance is one of the reasons banks are able to attract the deposits.

Insurance Fund

The FDIC’s fund, which fell into a deficit of almost $21 billion after a wave of bank failures, turned positive during the second quarter for the first time in two years, the agency reported this week. On April 1, the FDIC changed its formula for assessing premiums, increasing the cost for most large banks and adding to their deposit expenses.

That’s adding to the pinch on bank profits as revenue shrinks and yields on assets decline. Net interest margins, the difference between what banks pay to borrow and what they make on loans and securities, declined in the second quarter, "reflecting growth in low-yielding balances at Federal Reserve banks," the FDIC said Aug. 23 in its quarterly report.

European Crisis

U.S. deposits may surge again if Europe’s sovereign-debt crisis escalates and the region’s lenders face a funding squeeze. Most of JPMorgan Chase & Co.’s almost $53 billion in new deposits in the second quarter were tied to Europe, according to Pri de Silva, a New York-based analyst at CreditSights Inc. "If you are a bank you don’t want to use excess capital for these hot-money deposits," de Silva said.

Shares of the 24 U.S. firms in the KBW Bank Index have declined 28 percent this year. The second-worst performer in the index, Charlotte, North Carolina-based Bank of America Corp., lost half its value in 2011 before rebounding this week. Most lenders already have capital cushions well above the minimum of 5 percent that would trigger an order from regulators for corrective action, according to one of the people.

The Tier 1 leverage ratio for Bank of America, the largest U.S. lender, was 6.86 percent at the end of June, while JPMorgan stood at 7 percent, according to second-quarter regulatory filings. Citigroup Inc.’s leverage ratio was 7.05 percent at the end of June, and San Francisco-based Wells Fargo & Co.’s was 9.43 percent. Citigroup and JPMorgan are based in New York.

Changing Assets

If Citigroup’s average total assets changed by $1 billion, it would alter the leverage ratio by 0.4 basis points, while a $100 million change in Tier 1 capital would affect the leverage ratio by half a basis point, according to the bank’s second- quarter filing.

Relaxing the rules or enforcement could be a slippery slope, said Lou Crandall, chief economist at Wrightson ICAP LLC, a Jersey City, New Jersey-based unit of London-based ICAP Plc, the world’s largest inter-dealer broker. "Asking for a free pass on the leverage ratio for bank deposits by itself isn’t something that regulators would consider," Crandall said. "The question is whether banks should be able to exclude reserve balances since they are a risk-free asset."

UBS may start to charge banks for holding Swiss francs

by Reuters

Bank clients that keep large balances in the safe-haven currency will pay for the privilege

Swiss bank UBS may charge client banks a fee on cash accounts they use to clear transactions, it said on Friday, in a move to discourage them from using the accounts to hoard safe-haven Swiss francs. "Should we see a continuation of the net inflow of francs in cash clearing accounts of our banking customers, we might have to take corrective action … by means of a temporary excess balance fee," it said.

After record demand for the franc, UBS said it was monitoring franc cash balances in the current accounts of its franc clearing customers. The news helped the euro climb more than 2% against the franc to a one-month high . "This is a way to make investors pay for the privilege of owning the currency," said David Miller, fund manager at Cheviot Asset Management in London.

The move came amid speculation that Switzerland might consider imposing negative interest rates on Swiss franc deposits as it fights a surge in the franc to record highs against the dollar and euro this month.

Banks face $340 billion state-backed bond refi hole

by Helene Durand - IFR/Reuters

* Tough new issue markets could curtail banks' pre-funding plans

* New investors likely needed to replace government-guaranteed debt holders

* Concentrated refinancing burden poses additional risks

Banks will struggle to refinance the upcoming mountain of government-guaranteed debt that is due to mature in the next two years unless the primary market fully thaws in the coming weeks, according to bankers and investors. Banks had planned to aggressively use the autumn period to get ahead of large refinancing requirements in 2012.

Thomson Reuters data show that the USD230bn equivalent of European bank government-guaranteed debt will mature in 2012 and US banks will have more than USD122bn maturing. Governments started guaranteeing banks' debt issuance in September 2008 as capital and money markets froze after the failure of Lehman Brothers on September 15th. Most of the guarantees had a three-year maturity, although Spain and France allowed banks to issue up to five years.

"The wall of upcoming maturing government-guaranteed debt is a concern, especially if the current market freeze goes on for much longer and spills over into 2012," said Martin Lukac, financials credit analyst at Principal Global Investors. "If you look back, the government-guaranteed schemes were all established around the same time and were limited in terms of maturities which means that a lot of them are coming up at the same time, making the banks' maturity profile very frontloaded," said Lukac.

Pressure has built up in the financial sector. In recent weeks, fears that the euro zone sovereign debt crisis will spill over into banks has seen U.S. money market funds start to rein back the maturities they are willing to lend to them. "Bank treasurers know that next year is a big year for government-guaranteed refinancing and part of the reason why some of the larger funders in the market did so much at the beginning of this year was because a lot of them wanted to pre-fund some of next year's maturities in the autumn," Robert Kendrick, financials credit analyst at L&G.

"This was to mitigate a concentrated refinancing burden over the next couple of years, brought on by most government-guaranteed issuance being limited to 2012 or 2013, rather than being more evenly spread," said David Loughran, debt syndicate at Lloyds Capital Markets. The two biggest bank funding avenues, senior debt and covered bond issuance, have been largely shut since early July. "The problem is, issuance has now ground to a halt, and even if they were ahead at the end of June, they might now struggle to complete this year's funding," said Kendrick.

Market Shut Down

According to Thomson Reuters data, a mere USD7bn equivalent of senior was raised by European banks in July while the tally for August is even lower at just over USD1bn equivalent. This compounded poor volumes in June when USD17.4bn was sold, well below May' s figure at USD41.2bn. It's a similar story for the normally resilient covered bond sector, where ING Bank's announcement on Wednesday that it was planning a 10-year euro offering was the first benchmark launched since early July when EUR8.1bn was raised. So far, the tally for the whole of August is a mere EUR1.2bn.

Financial indices have performed very poorly in recent weeks, according to Markit, its Senior Financial index hit a record wide of 260bp on Tuesday. It is not just a matter of the large refinancing size that will be a challenge. Another will be finding investors in bank debt.

"A problem that bank treasuries have been working to avoid is a number of the people who bought government-guaranteed debt won't buy anything else," said Lloyds's Loughran. "So it's not as if the market will get a liquidity event and have cash to put to work in bank paper. For some of these investors, even a Triple A RMBS or covered bond won't necessarily float their boat."

Banks' pursuit of new investors will be hindered by fears of haircuts on senior debt: the debate on senior bondholder bail-in will return in the autumn when the European Commission releases its legislative framework on banks' resolution and recovery.

Meanwhile, investors are likely to demand higher premiums in order to protect from volatility as good new issue performance is not guaranteed given the market backdrop and the lack of solution to the European sovereign crisis. "If we were to see a new issue from a bank, the issuer would have to offer a substantial new issue premium," said Lukac. "We would also expect demand for new deals to be diminished given that US-based accounts are currently not adding European risk and this can really be felt in the market."

L&G's Kendrick added that said that while some of the current concerns in the market were somewhat unjustified, he would be reluctant to put cash to work right now. "Selling a senior deal is very hard right now and in order to buy, we would need to have confidence that a deal will perform and not be 50bp wider the following week," he said.

While the refinancing numbers drop off dramatically in 2013 and 2014, European banks' still have USD41bn and more than USD94bn coming up to maturity in 2013 and 2014. Furthermore, as much as USD63.8bn of European government-guaranteed bank debt is maturing before year-end and USD49.5bn for US banks.

More Transparent Bank Stress Tests Are Needed

by Simon Johnson - New York Times

Europe and the United States both need to conduct another round of stress tests on their banks, with a model similar to what was done in the United States in 2009, but with a more negative downside scenario — in particular, assessing the effects of a major sovereign debt problem in the euro zone.

The point of such a scenario is to determine how much equity financing banks need to have if the world economy turns ugly. If the big banks raise more capital in advance, we are less likely to see economic downturn again become financial catastrophe.The prevailing wisdom about Europe is that it faces primarily liquidity problems. In this view, a few of the larger countries have had trouble rolling over their debts, and some leading banks need help with short-term financing. The European Central Bank can assist with both by buying government bonds and lending to banks and, in the most optimistic interpretation, the consequent political discussions will help strengthen European Union integration.

There are two problems with this positive spin on recent events. The first is that sovereign debt problems can easily become solvency issues — that is, more about whether countries can afford to service their debts rather than whether they can raise enough cash at reasonable rates in any given week. The key issue is growth — if Italy, Spain and others can show they will grow reasonably quickly, then debt relative to gross domestic product will decline, and rosy projections will be back in fashion.

But if signs of growth do not return soon, perhaps over three to six months, the next downward revision to forecasts will spread deeper debt pessimism. And any markdown for global growth prospects, including for reasons outside Europe’s control (such as overheating in China’s residential property market), would also not be helpful over the coming year. My Peterson Institute policy paper with Peter Boone in July suggested some potential escape routes, but the summer so far has produced only further attempts to muddle through.The more immediate Achilles heel is banking. The virtues of big European banks were extolled by some Congressional representatives during the Dodd-Frank legislation in spring 2010. What a difference a year makes; not many members of Congress would today endorse anything about European banking, given all the problems that have emerged.

The main immediate problem for Europe is that we still don’t know exactly the condition of its major financial institutions. The Europeans have run bank stress tests twice recently, in mid-2010 and again earlier this year. But in both cases the tests were far too lenient and banks were not required to raise enough capital.

They should have been compelled to increase their equity funding relative to their debt, in order to create a greater buffer against future losses.

The 2009 banking stress tests in the United States can also be criticized for not including a scenario that was sufficiently negative. In recent weeks the market has expressed great skepticism about Bank of America, its inherited liabilities, future business model and, most of all, the adequacy of its capital.

Most likely, Bank of America needs to be broken up, with the continuing businesses funded with equity to a level that could withstand adverse legal outcomes and a deep recession. Warren Buffett’s investment in the bank, announced this morning, may be in a step in the right direction. (For more background on how to think about bank equity, see the recent testimony of Paul Pfleiderer to the financial institutions subcommittee of the Senate Banking Committee; anyone working on banking policy in Europe or the United States should read this.)

Dodd-Frank created pre-emptive intervention powers, at the behest of Treasury and the Federal Reserve, with part of the rationale being that these could be used to prevent a megabank’s slow death spiral from becoming a market panic.

In “13 Bankers,” James Kwak and I expressed considerable skepticism that this could work — it just does not fit with the history and politics of regulation in the United States, within which even the Treasury secretary defers to what Bloomberg News calls the "Wall Street Aristocracy."

The American 2009 Supervisory Capital Assessment Program, known as SCap (pronounced ESS-cap), was designed to reveal potential stressed capital levels and, as a result, the 19 companies covered by SCap have since increased their common equity by more than $300 billion.

Unfortunately, weakness at Bank of America generates systemic risk, undermines overall market confidence and magnifies the risk of another recession; this is exactly what SCap is supposed to have avoided — but failed to do because it was not sufficiently tough.

The Comprehensive Capital Analysis and Review stress tests, known as CCar (pronounced SEE-car), concluded in April 2011, were even less helpful. These were much less transparent, focused more on companies’ internal capital planning processes. The Fed did sensitivity analysis of the companies’ own stress tests; this is not exactly reassuring, given how badly the industry’s own models have failed in the recent past — including in the events that led up to the Fed’s $1.2 trillion of emergency loans in 2008.

Yet the European stress tests to date must be rated a notch or three below even the CCar in terms of transparency and communication of information that allows market participants to make informed decisions. The latest round, conducted by the European Banking Authority through July 15, did not even examine what would happen if a sovereign borrower had to restructure its debts — exactly what Greece was working on during the same time frame. (To be precise, there was some "sovereign stress" in the tests but very little compared with what we have seen and could see.)

This is worse than embarrassing. It creates exactly the wrong kind of uncertainty around European megabanks, including their operations in the United States and potential spillover effects.

In part this happened because the European Banking Authority is new — it came into existence on Jan. 1 — and not sufficiently powerful relative to national bank supervisors, many of whom are stuck in an old mindset where transparency is bad and full disclosure of banks’ balance sheets is scary. (The low capital levels of European banks was described more fully this week in a Bloomberg article.)

But partial facts and distorted information flow are exactly what creates fear and instability, not just in Europe but much more broadly.

If euro-zone leaders want to make any progress on governance reform, they should immediately strengthen the banking authority and call for a new round of stress tests. These tests should include a deep recession scenario in Europe, as well as disruptions to sovereign debt financing. At the same time, the Federal Reserve should acknowledge that the CCar was not enough; it’s time for a new round of tough stress tests here, as well.

The notion that bank equity is socially expensive and should be minimized is an idea whose time has passed — as Anat Admati, Peter DeMarzo, Martin Hellwig and Professor Pfleiderer have argued. It is time to find ways to strengthen the equity funding of major financial institutions around the world, quickly, fairly and effectively — a point that was made clear in the recent hearings held by Senator Sherrod Brown, Democrat of Ohio.

Any further delay risks worsening the global slowdown.

Bernanke Is Signaling An Announcement On September 21

by Bruce Krasting - My Take On Financial Events

I went to play golf this morning rather than listen to the Bernankster. After all, I knew what he was going to say. I read about the speech in the Wall Street Journal a day before.

I (and many others) have made note of the fact that the WSJ’s crack reporter, Jon Hilsenrath, is the mouthpiece for Big Ben. This is what Jon said had to say last night. Do you think he talked to Bernanke before he wrote this? (15 hours before speech time)Federal Reserve Chairman Ben Bernanke isn’t likely to break much new monetary-policy ground in his Jackson Hole speech Friday

To be sure, a number of others who have a public view on Fed policy also commented that the speech from the Chairman would bring nothing new. But the consistency of Hilsenrath’s words and Bernanke's actions is no coincidence.

If you believe that Hilsenrath gets the whisper from Ben, then you might want to consider what Jon had to say after the speech was delivered:Fed policy makers will be discussing their options at a September policy meeting which has been expanded to two days instead of one to explore whether the Fed should do more.

Jon then quotes from the speech:“The committee is prepared to employ its tools as appropriate to promote a stronger economic recovery.”

Then Jon tips Bernanke’s next move:it is worth remembering, when the Fed has said it is prepared to act during this long-running economic crisis, it generally has acted.

Bernanke is tipping his hand (via Jon) in order to prepare the market for what is to come in a few weeks. This is a heads up to the insiders that more monetary gas is in the works. The stock market’s first reaction to today’s non-event was to sell off hard. But after the word got around that this was just a delay (and a short one at that) stocks caught a bid. Basically, the plan by Bernanke to leak his intentions worked.

I think there are two reasons that Bernanke chose not to announce policy changes at Jackson Hole:

I) He wants it to look to the world (and a few Republican politicians) as if the Fed’s actions are being done only after deep deliberation and discussion. That is why the next meeting has been changed to a two-day format.

There will be a two-day circus of Fed Governors looking very serious. But that is just for the TV audience. This is Ben’s show. He has the votes. He is steering the ship. The decisions have already been made. Ben’s going to do something on 9/21.

II) Ben had to put off announcing more monetary oomph today because there is something that has to happen first. There has to be something that comes out of the EU before Bernanke makes his next move.

I’m not sure what happens next in Europe. I’m of the opinion that something needs to be done, and it needs to be done quickly.

There are a number of things that the ECB could do. They could (1) significantly expand their effort at QE (the number starts at E 1 trillion). They could (2) drop official lending rates close to zero. They could (3) agree to issue E bonds.

Some combination of those actions would buy some more time. The problem is that all of those steps have been discussed and pretty much firmly rejected. There is a fourth option. The strong hands in the EU could give in to the markets and let some of the PIIGS (starting with Greece) float on their own. This option has also been previously rejected.

I think it is time for serious consideration for this. I can’t think of a single person who has a voice in these matters that actually believes that Greece can be saved with more debt. We shall see, possibly as soon as Sunday night.

Yet another option is to get the US Fed into the picture with dramatic draw-downs on existing USD swap lines (Starts with $500 Billion). This is another possibility for this weekend or next.

My last point is one that I have made many times before, but feel obligated to repeat.I flat out hate that this Fed is conducting monetary policy through leaks, a wink and a nod and innuendo.

There is far too much at stake to make a circus out of the process. It feels like we should just put up a tent, because a three-ring circus is what we are getting non-stop. And Bernanke is the strong man in the middle ring.

Big Asset Sale Near at Bank of America

by Nelson D. Schwartz - New York Times

Bank of America is completing plans to sell more than half of its stake in the China Construction Bank in a deal that could raise nearly $10 billion, just a day after Warren E. Buffett invested $5 billion in the beleaguered American financial giant.

A consortium of sovereign wealth funds in Asia and the Middle East as well as several private equity firms are in negotiations with bankers and could close a deal by early next week, two officials briefed on the talks said Friday. While Bank of America plans to sell at least half of its 10 percent stake in the Chinese bank, it is willing to unload much more than that for the right price, according to the officials, who spoke on the condition that they not be named because the sale was still being negotiated.

The sale would improve Bank of America’s capital position under international Basel III regulations. Bank of America’s stock fell by nearly 30 percent earlier this month on investor fears that it would have to sell more shares to raise more capital amid huge losses on soured mortgage securities and a weakening economy.

Mr. Buffett’s investment — and the likely sale of the Chinese stake — have helped allay those worries while reinforcing investor confidence in management, and Bank of America shares rose 1.4 percent to $7.76 a share on Friday. The stock jumped more than 9 percent Thursday on news of Mr. Buffett’s move. A Bank of America spokesman declined to comment.

But if a deal is completed soon, it would also defy speculation that deep-pocketed buyers would be hard to find at a time of intense volatility in the markets and uncertainty about the global economy.

The sale by Bank of America has also been complicated by the fact that other institutions have been selling shares in China Construction and other Chinese banks. In July, Singapore’s state investment fund, Temasek Holdings, sold more than $1 billion worth of shares in the China Construction Bank.

Unloading the Chinese shares represents one more step in reversing the legacy of Bank of America’s former chief executive, Kenneth D. Lewis, who made Bank of America the nation’s largest bank through a long series of acquisitions, some more profitable than others. One in particular, the 2008 purchase of Countrywide Financial, the subprime lender, has been disastrous, costing the bank more than $30 billion.

The investment in the China Construction Bank, which began in 2005, has been much more successful. In its latest filings with the Securities and Exchange Commission, Bank of America estimated the entire stake was worth almost $19.6 billion, about $10 billion more than it paid. Bank of America owns 25.6 billion shares of China Construction, of which 23.6 billion are covered by a lock-up preventing sales that expires on Monday. A lock-up on the remaining 2 billion shares expires next August.

For Bank of America, unloading the China Construction stake is also part of a broader effort by its chief executive, Brian T. Moynihan, to sell off noncore businesses, strengthen the bank’s capital position and focus on the company’s retail and investment banking operations. Since the start of 2010, Mr. Moynihan has sold more than $30 billion worth of assets, most recently unloading the bank’s Canadian credit card business and a portfolio of commercial real estate. The potential deal was first reported by CNBC.

While Mr. Buffett’s move and the potential sale of China Construction have been greeted positively by investors, the overhang from Countrywide still looms large. In June, Bank of America reached an $8.5 billion settlement with 22 major holders of soured mortgage securities to help cap future repurchase claims. That deal was set to be reviewed by a state court judge in November, but a group of other investors who oppose the settlement filed a notice Friday to move the case to federal court in Manhattan.

If that effort were to ultimately succeed, it could delay resolution of the settlement, but legal experts said permanently moving the venue would not be easy. The trustee for the 22 investors, Bank of New York Mellon, is expected to ask next week that the case be kept in state court. The state court had imposed a deadline of Tuesday for any objections to the agreement.

As Trade Volumes Soar, Exchanges Cash In

by Graham Bowley - New York Times

The latest financial market convulsions have been tough for almost everyone, including traders caught on the wrong side of another big swing and pained everyday investors watching their dwindling holdings go down and up — and down again.

But there is a silver lining to even this latest market horror show, at least for the exchanges where the financial instruments change hands. Businesses like the New York Stock Exchange and the Chicago Mercantile Exchange skim cents off each stock or contract bought or sold over their trading floors or computers. With the daily volumes of financial market contracts sent surging through their systems by nervous traders and investors up by billions, the latest trading rush is directly polishing their bottom line.

The effect, however, may be fleeting. The rising volumes have generally not translated into higher stock prices for the exchanges, and they and some analysts are worried that the volatility and downbeat economic news may frighten away investors in the long term. "Volume is positive on a short-term basis but because it is based on negative macroeconomic factors, these volumes are not necessarily sustainable," said Joseph M. Mecane, executive vice president for cash trading at NYSE Euronext, which operates the New York Stock Exchange.

The latest swings came Friday when the Standard & Poor’s 500-stock index fell 2 percent in the morning, but climbed back up in the afternoon to finish 1.5 percent higher, as investors digested remarks by Ben S. Bernanke, the Federal Reserve chairman, that left the door open to further support for the economy. The Dow Jones industrial average swung about 363 points during the day, closing up 1.2 percent, to 11,284.54.

Across United States stock markets — including the big electronic exchanges like Nasdaq, BATS and Direct Edge — trading volumes so far in the latest quarter are 17 percent ahead of the same period last year, according to figures from Credit Suisse. Volumes have been hitting levels almost double what they normally are at this usually quiet time of year, Mr. Mecane said.

Markets have been sent wild this summer amid a number of exceptional events, like the showdown over the debt ceiling in Washington, the downgrade by the credit rating agency Standard & Poor’s of the United States’ long-term debt on Aug. 5, the global fallout from Europe’s debt crisis and a raft of data pointing to a stalling United States economy. On a couple of days earlier in August, stock market volumes touched about 15 billion daily trades, although volumes are now back to about eight billion or nine billion daily.

The stock exchanges on average charge 3.5 cents for every 100 shares traded, according to Credit Suisse. That has declined in recent years with greater competition between the exchanges, so the pop in volumes is not delivering as much to them in increased profits as it would have just a few years ago. The exchanges have also diversified into other business like providing trading technology to banks. That means revenue from stock and derivatives trading accounts for a smaller proportion of overall income. In the case of Nasdaq, for example, it makes up a third of overall sales.

The exchanges, most of which are public companies, generally will not comment on the effect these increased volumes will have on profits. But analysts like Howard Chen, a financial analyst at Credit Suisse who watches the exchanges, said that because volumes were already tracking 15 to 20 percent above what he had been expecting, earnings should be up a similar amount.

It’s not just the stock market that is experiencing a lift. Traders have been busily betting on interest rates, commodities, currencies and even volatility itself. The Chicago Mercantile Exchange where these and other products like United States Treasury futures are in large part traded has recorded a big pick-up in trading volumes recently.

Aug. 9, for example, was a record day for the Chicago exchange, when nearly 25.7 million contracts were traded, beating the last record, which was during the so-called flash crash on May 6 last year, when 25.3 million contracts were traded, the exchange said. So far during the third quarter, volumes on the Chicago exchange are up 39 percent compared with the same period a year ago, Credit Suisse said.

Futures in gold, oil and the broad stock market index, the S.& P. E-Mini, are all up. In an era when volatility has become the new norm, another instrument that has had a surge in volumes is the Chicago Board Options Exchange Volatility Index. The VIX, as it is known, measures the short-term implied volatility of options on the S.& P. 500. Financial instruments based on the VIX are traded both electronically and in the exchange’s trading pits in Chicago — where there is a special VIX pit, and 60 dedicated VIX traders.

It is also called the fear index, and as the S.& P. 500 has spiraled down and up, VIX futures and options have become a popular tool for all sorts of fearful investors to protect themselves against the swings — and maybe even make a little money. "Volatility in itself is becoming a more popular and investable asset class for institutions and also for retail investors," Mr. Chen said.

Volume in VIX options is up 79 percent and trading in futures on the index soared 290 percent through Aug. 19. Futures trading this month is already a record, surpassing July, which was the next highest. The single busiest day on record was Friday, Aug. 5, when 1,194,468 options contracts were traded. "When volumes are up we do well," said William J. Brodsky, chairman and chief executive of CBOE Holdings.

Mr. Brodsky said the VIX was created with professional investors in mind but is increasingly being embraced by retail investors to protect against volatility. The VIX generally moves in a range of 15 to 50, although it reached 80 during the financial crisis in 2008. Investors worried that their stock holdings were vulnerable to a sell-off in the market, for example, might buy the VIX as protection because the VIX would most likely rise.

Mr. Brodsky said a couple of dozen VIX exchange-traded notes are now offered by banks like Barclays. They were linked to the VIX and aimed at providing easier access for ordinary investors. The strange thing is the heightened market volatility has not been particularly good for the exchanges’ own share prices.

Even as their volumes have rocketed, their own stock prices have languished. While CBOE’s shares are up 7 percent this year, the Chicago Mercantile Exchange’s stock price is down 22 percent. NYSE Euronext’s share price is down 9 percent for the year, and stock in Nasdaq is down 4 percent. "It’s a little odd," Mr. Chen said.

One reason might be that even though volumes have been picking up in recent years, the rates the exchanges charge at least for stock trading have come under pressure. Another reason, according to Mr. Chen, is the possibility — however distant — of a financial transaction tax raised by European policy makers, which would depress trading volumes. But perhaps the biggest reason is that the markets really think this is the "storm before the calm," he said — that soon all this volatility will go away and trading will be becalmed, perhaps even more so than before. That won’t be good news for the exchanges.

Other industry analysts agree. They fear that the big swings will hurt investors’ confidence in the markets and keep them away in the future. The same thing happened last year in the stock market. After the flash crash on May 6 — another time when Europe’s debt crisis was roiling world markets — May and June were busy months, but then volumes slowed markedly, partly because ordinary investors were frightened away, he said.

Stock market volumes increased for six consecutive years between 2004 and 2009 but then fell 13 percent between 2009 and 2010. This year, despite the latest bounce, volumes across the entire stock market are 7 percent lower compared with last year.

High street recession worst for 40 years, says Co-Op chief Peter Marks

by Louise Armitstead - Telegraph

The recession on Britain's high street is the worst for more than 40 years, the boss of the Co-operative Group has claimed, as shares in a trolley-full of retailers plunged.

Peter Marks said that for the first time people have been cutting food budgets - normally an area that is relied upon as "recession-proof". "People are spending less on food – that's a first," said the Co-op's chief executive. He added that he and other retailers are having to cut prices radically to shift stock. While normally around a quarter of products are on promotion, approximately 40pc are discounted at the moment, Mr Marks said. He added: "We're not into 'buy one, get one free' – we're into 'buy one, get two free'."

He added: "It has been a tough six months, the toughest I've ever experienced in my 40 years of retailing. I don't think we have come out of recession since 2008… I've operated through several recessions – this is by far the longest." The Co-Op, which is Britain's fifth biggest supermarket group, unveiled a fall in first-half pre-tax profits to £230.8m. Group sales fell from to 6.89bn in the six months to July, down from £6.95bn during the same period last year. Food sales were £3.7bn, 4.6pc lower than last year.

Mr Marks warned profits were unlikely to improve by the full year. "I really don't see any light at the end of the tunnel," he said. His gloom was reflected across the high street. Topps Tiles, the UK's biggest tile and wooden floor specialist, issued a profits warning, sending the shares plunging 13? - 29pc - to 33p. Matt Williams, chief executive, said he has seen a "step down in consumer confidence since the beginning of July".

Topps Tiles, which employs 1,600 people in the UK, said revenues dived by 10.4pc in the first seven weeks of its fourth quarter. Mr Williams warned that jobs could go: "With fewer sales in store, it's difficult to argue with the logic that we need fewer people to service those sales."

A range of retailers were punished on the stock market. Clinton Cards tumbled 10pc; JJB Sports was down 7pc; Marks & Spencer fell 4pc; and Kingfisher, the owner of B&Q, was off more than 3pc.

The CBI's latest quarterly Distributive Trades Survey found 46pc of retailers said sales had fallen in the two weeks to August 16th with only 13pc recording a rise. The trade body said that retail sales volumes had fallen at the fastest rate for a year. According to the survey, retailers are more negative now than at any time in the past 18 months about the immediate prospects for sales growth.

Judith McKenna, chairman of the CBI's survey panel and chief operating officer of Asda, said: "August was a tough month on the high street. Sales volumes fell at a pace not seen in more than a year, as consumers have continued to see their real incomes squeezed by a combination of inflation and weak wage growth."

The Kingdom of Magical Thinking

by Robin M. Mills - Foreignpolicy.com

Widely assumed to be a fabulously wealthy welfare state, Saudi Arabia is in fact an economic basket case waiting to happen.

In 1935, an oilman visiting the Middle East reported back to his headquarters, "The future leaves them cold. They want money now." Although the temptation of overspending has repeatedly undermined oil-rich governments from Caracas to Tehran, Saudi Arabia avoided this trap over the last decade through fiscal discipline that has kept its expenditures below its swelling oil receipts.

But in a recent report striking for the candor of its unpalatable conclusions, Saudi investment bank Jadwa laid out the kingdom's inexorable fiscal challenge: how to balance soaring government spending, rapidly rising domestic oil demand, and a world oil market that gives little room for further revenue increases. And that was before the recent economic turmoil knocked $20 per barrel off oil prices.

Saudi Arabia's government spending, flat since the last oil boom in the 1970s, is now rising at 10 percent or more annually. And it will rise faster still: The House of Saud's survival instinct in the wake of the initial Arab revolutions led King Abdullah to announce $130 billion of largesse in February and March. The resulting increases in government employment and salaries can be cut only at the cost of more discontent.

And that's only what the kingdom is spending on its "counterrevolution" at home. Saudi Arabia will pay the lion's share of the pledged $25 billion of Gulf Cooperation Council aid to Bahrain, Egypt, Jordan, and Oman. With Iraq, Syria, and Yemen likely flashpoints yet to come, the bill will only increase. Already, nearly a third of the Saudi budget goes toward defense, a proportion that could rise in the face of a perceived Iranian threat.

Meanwhile, fast-growing domestic demand poses a serious threat to oil-export revenues. The kingdom is one of the world's least energy-efficient economies: With prices fixed at $3 per barrel for power generation and $0.60 per gallon of gasoline, Saudi Arabia needs 10 times more energy than the global average to generate a dollar of output.

Subsidized natural gas, too, is in short supply, undermining an economic diversification drive focused on petrochemicals. As much as 1.2 million barrels per day (bpd) of oil are burned for electricity to meet summer air-conditioning demand, yet Jeddah, Saudi Arabia's second-largest city, still suffers frequent power cuts. By around 2026, Jadwa projects that domestic consumption will be over 5 million bpd, exceeding exports, which will never again reach their 2005 peak.

This combination of higher spending and lower exports shortens Saudi Arabia's time horizon. Usually considered, on shaky evidence, to be a "price moderate" within OPEC, the kingdom now requires $85 per barrel to balance its budget. That figure will rise to $320 by 2030, according to Jadwa. (Of course, just because the Saudis need a certain oil price to balance the budget does not mean they can get it. Higher prices today come at the inevitable cost of future revenues, as economic growth is reduced and consumers choose more efficient vehicles.)

Savings cushion the budget for now. But the experience of the last oil price cycle is likely to recur: $180 billion of assets in 1980 had become $176 billion of debt by the end of 2002, and despite the oil-price crash, Riyadh was able neither to cut spending nor to grow a viable non-petroleum economy. This time, Jadwa foresees that the Saudi Arabian Monetary Agency will be forced to draw down its $500 billion of foreign assets to the point where, by 2030, the country's fiscal position will be under severe strain.

So far, the kingdom has been fortunate. This decade's rapidly rising spending was enabled when Saudi Arabia's main OPEC rivals, Venezuela, and Iran, left the field clear due to underinvestment in and mismanagement of their oil industries. Along with the war in Libya, this has allowed Saudi production to increase to its highest level in 30 years while prices have remained strong. But the good times will soon come to an end.

Oil prices have again, as in 2008, been allowed to get too high, too fast. The renewed economic downturn, combined with fears of overheating in China and other emerging markets, has only sharpened this challenge. Growing efficiency, demographics, and alternatives mean that OECD oil demand is probably in a slow, long-term decline, while non-OPEC supply is proving more robust than expected, with strong growth in Brazilian pre-salt oil and North American unconventional shale oil and oil sands.

And, for the first time since Oil Minister Ahmed Zaki Yamani did battle with the Iranians in the 1970s, Saudi Arabia faces a real challenger within OPEC. Even if Iraq's ambitious plans are only half-realized, it will soak up more than half of global demand growth. Its vast, low-cost reserves make major production increases attractive even if they reduce prices. For its own reasons, Iran seeks to undermine Iraqi stability, but that would hardly be a palatable outcome for the Saudis either.

And that's not all: Angola also has room for further growth; Muammar al-Qaddafi's impending defeat may restore some of Libya's production; and, with Hugo Chávez suffering from cancer, Venezuela's oil policy may change after the 2012 election.

The Saudis' dilemma is this: They hold nearly all OPEC's spare capacity, their essential weapon for keeping the cartel in line. June's "worst meeting ever" was actually a victory for Saudi Oil Minister Ali al-Naimi. Opposition by Iran, Venezuela, Libya, and others to a production hike left him free to increase output as far as he chose. Yet Saudi Aramco, the country's monopoly state oil company, has few drill-ready development projects. Plans announced in 2008 to take Aramco's capacity to 15 million bpd have not been implemented, and the only big project under way, the giant Manifa heavy oil field, with about 900,000 bpd, will mostly serve domestic needs.

So what should the Saudis do? Setting a credible target, say $70 per barrel, and defending it by creating new spare capacity would reduce long-term prices. By enduring some pain themselves and drawing down their vast savings, they would burn off high-cost competition, punish OPEC rivals that are ignoring quotas, and damage archenemy Iran. Yet they are understandably reluctant to spend billions of dollars on new fields at a time of wavering demand.

Ambitious plans for nuclear and solar power are no panacea. Saudi Arabia has no competitive advantage over other countries in alternative energy. If it succeeds in reducing oil use in transportation, other countries can too -- so who will be buying Saudi oil?

The black hole in current policy discussions is improved energy efficiency. Raising domestic fuel prices would cut demand, allow development of higher-cost gas resources, and free up more oil for export. "Smart" subsidies or cash transfers could offset the price hikes for vulnerable groups.

A lower oil-price target would have to be combined with domestic spending restraint. The Saudi government cannot forever be the employer of last resort; reshaping education and labor policy to bring more Saudi citizens into the private sector would ease some social pressures. Between 2005 and 2009, 2.2 million private-sector jobs were created, but only 9 percent went to Saudi citizens.

Tinkering is not enough. Without radical reforms, Saudi leverage within OPEC will be increasingly constrained. The kingdom's regional power will weaken, precisely at the time when it is attempting to step up its role. And in the long term, its economic and social model will come under intolerable strain.

Yet the crisis is still too far away, the lure of easy oil money too strong -- and the policy changes required demand deft execution untypical of Saudi bureaucracy. As Machiavelli cautioned, "There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things."

Time to Get Angry, Europe

by Ulrich Beck - Spiegel

The European common currency is in trouble, several EU countries are facing mountains of debt and solidarity within the bloc is declining. It is European youth, in particular, who have drawn the short stick. Closer cooperation is the only way forward.

Germany's European policy is about to undergo a transformation as significant as Ostpolitik --the country's improvement of relations with the Soviet bloc -- was in the early 1970s. While that policy was characterized by the slogan "change through rapprochement," Berlin's new approach might be dubbed "more justice through more Europe."

In both cases, it is a question of overcoming a divide, between the East and the West in the 1970s and between north and south today . Politicians tirelessly insist that Europe is a community of fate. It has been that way since the establishment of the European Union. The EU is an idea that grew out of the physical and moral devastation following World War II. Ostpolitik was an idea devoted to defusing the Cold War and perforating the Iron Curtain.

Unlike earlier nations and empires that celebrated their origins in myths and heroic victories, the EU is a transnational governmental institution that emerged from the agony of defeat and consternation over the Holocaust. But now that war and peace is no longer the overriding issue, what does the European community of fate signify as a new generational experience? It is the existential threat posed by the financial and euro crisis that is making Europeans realize that they do not live in Germany or France, but in Europe.

For the first time, Europe's young people are experiencing their own "European fate." Better educated than ever and possessing high expectations, they are confronting a decline in the labor markets triggered by the threat of national bankruptcies and the economic crisis. Today one in five Europeans under 25 is unemployed.

A New Age of Risky Confusion

In those places where they have set up their tent cities and raised their voices, they are demanding social justice. In Spain and Portugal, as well as in Tunisia, Egypt and Israel (unlike Great Britain), they are voicing their demands in a way as nonviolent as it is powerful. Europe and its youth are united in their rage over politicians who are willing to spend unimaginable sums of money to rescue banks, even as they gamble away the futures of their countries' youth. If the hopes of Europe's young people fall victim to the euro crisis, what can the future hold for a Europe whose population is getting older and older?

News programs offer new visual material for the dawning of a new age of risky confusion -- the "world risk society" -- on an almost daily basis. The headlines have been interchangeable for some time: Insecurity Over the Future of the Global Economy, EU Bailout Fund in Jeopardy, Merkel Attends Crisis Meeting with Sarkozy, Rating Agency Announces Downgrade of US Debt. Does the global financial crisis signal the deterioration of the old center? Ironically, it is authoritarian China that is playing the moral apostle on the financial front, with its sharp criticism of both democratic America and the EU.

There is one thing the financial crisis has undoubtedly achieved: Everyone (experts and politicians included) has been catapulted into a world that no one understands anymore. As far as the political reactions are concerned, there are two extreme scenarios that can be juxtaposed. The first is a Hegelian scenario, in which, given the threats that global risk capitalism engenders, the "ruse of reason" is afforded an historic opportunity.

This is the cosmopolitan imperative: cooperate or fail, succeed together or fail individually. At the same time, the inability to control financial risks (along with climate change and migration movements) presents a Carl Schmitt scenario, a strategic power game, which opens the door to ethnic and nationalist policy.

Taking Europe for Granted