“Main timber slide at Ottawa, looking toward Canada’s parliament buildings. The men are riding a timber crib, which would carry up to 50 logs tied together down the chute. The logs were on their way to Montreal for shipment overseas"

Stoneleigh: As I travel around and visit many different places, the disparity in the speed at which the credit crunch is unfolding in different places is readily apparent, and with it the attitudes of local people to warnings of hard times to come. In places where the bursting of the credit bubble is more advanced, such as Ireland, people are generally more interested in understanding what went wrong and what they can do for themselves and their communities. In such places, where homes may already only be worth 40% of the mortgage on them, there is more public recognition and discussion of the issues, even if there is still a great deal of collective denial.

In other places where the impact of the bubble has yet to be felt, for instance Canada, where I am currently, there is still a sense of invulnerability. We haven't got as far as denial yet. That's hardly surprising when you can't tell a crack-shack from a mansion in places like Vancouver. This is bubble psychology at its most extreme, where no one cares what they pay for something, because they think someone else will always pay more, and no one cares what they owe, so long as the monthly payment is manageable in the short-term. Most other Canadian cities are still in the grip of bubble psychology as well, although not to the same extent. Needless to say, the level of public discussion in Canada is abysmally low.

The psychological contrast between Ireland and Canada is stark indeed. Ireland had one of the worst housing bubbles in the whole world. When I used to spend a lot of time there in the early 1990s, it was a sleepy agricultural place where no one seemed to have two cents to rub together, but they were the happiest people I knew. Interest rates had always been relatively high, so borrowing large amounts of money was not affordable. People had no access to the cheap credit that allows purchasers to bid up property prices with gay abandon. Access to land ownership had always been quite limited, with ownership concentrated in relatively few hands. Divorce was not only illegal, but unconstitutional, partly to avoid the break up of land parcels.

Irish property prices were a fraction of what they were in most parts of England at the time. In fact, local authorities in England were trying to escape their duty to house their own populations in council properties by buying them a cheap house in Ireland, instead of continuing to rent them one in England. The maintenance bill for decrepit council housing was so large that buying council tenants off with an Irish house made financial sense.

When Ireland joined the eurozone, interest rates plummeted to levels the Irish hadn't seen before. All of a sudden, people had access to cheap credit, and the EU pumped in enormous amounts of money (some 17 billion euros since the advent of the euro) for upgrading infrastructure. The Celtic Tiger was born, and the long-standing Irish diaspora went into reverse, with the addition of a wave of new immigration from Eastern Europe.

What followed was a staggeringly large property bubble, fuelled by extremely cheap credit that gave rise to almost insatiable demand. Property prices rose by a factor of 15 in 15 years. For a few years, the Irish were called the second richest people in the world (after Icelanders, who had managed to turn their entire country into a hedge fund in an even bigger credit boom). This is not riches, however. This is simply accumulating a veneer of material prosperity at the cost of digging oneself into an inescapable debt trap.

Since the Irish real estate bubble peaked and burst in 2007/2008, prices have plummeted and the Irish banking system has been plunged into crisis. The state guaranteed all deposits - a promise which it could not possibly afford to keep in reality. It pumped some 22 billion euros into a bank bailout (far more in one fell swoop than all the funds pumped in by the EU since Ireland joined, making EU membership a net negative for Ireland). With the scale of the banking woes becoming increasingly obvious, the government set up NAMA (the National Asset Management Agency) in 2009, with a view to using taxpayers' money to assume ownership of troubled property assets:

The idea is that the NAMA "will buy all of the land and property development loans of the six Irish banks of covered by the State guarantee. This means the total potential value of the loans which will be taken on by NAMA will be between €80 billion and €90 billion. By taking problem property loans off the hands of the banks, the Government hopes to put those institutions in a position where they can resume lending.

NAMA will probably become the biggest landowner in Ireland. Developers might not yet realise it – but every single land and investment property they own which has outstanding debt could end up in the new National Asset Management Agency. Even if these debts are bought by Nama at two-thirds of their face value – the bill could be in the region of €60 billion. (Ireland’s national debt is currently €54 billion.)"

This is a monumental transfer of public assets into private hands through a privatized-profits-but-socialized-losses model. The concentration of property ownership in Ireland is returning with a vengeance. With ordinary people having spent unpayable amounts to buy real estate, they are now likely to forfeit their property to the wealthy, who will buy it up from NAMA at a few eurocents on the euro.

This is the property ownership model that gave Ireland the great famine (an Gorta Mór - the Great Hunger of 1845-1852), when wealthy landowners continued to export food while half the tenant population either starved or emigrated. The population is still nowhere near what it was in 1850 as a result. Highly concentrated property ownership, with its concurrent gridlock on political power, risks an isolated elite acting purely in its own short-term interests, no matter what the consequences to the rest of the population.

It is quite possible, indeed likely, that Ireland (and other highly indebted states of the European periphery) may leave the eurozone, causing an enormous wave of economic dislocation, which would compound the impact of on-going credit crunch. While I don't see the periphery being forced to leave by other member states, I do see the austerity measures required to remain part of the club becoming so onerous that implementing them domestically would become a recipe for political suicide. Leaving the eurozone is no panacea though. Ireland is inevitably looking at a long period of extreme socioeconomic and political upheaval no matter what decisions its politicians make now.

Canada should be looking at Ireland for lessons on what the bursting of a major real estate bubble looks like, and the consequences of personal indebtedness. We too, over many years, have thrown caution to the wind when it comes to being offered the 'opportunity' to dig ourselves in over our heads:

Canadians' Personal Debt at Historic LevelAs interest rates drifted to the lowest levels in decades, consumers responded by buying everything from homes and cottages to cars and appliances. The shopping spree has fed a healthy cycle of economic growth and a robust job market - but we've gone deep into hock to pay for the good times. With every drop in interest rates, the definition of living within one's means changed - with financing like this, you too can afford a luxury condo! The notion of buying only what you could easily pay for became a meaningless principle.

Personal debt in Canada has been described as a Ticking Time-Bomb:

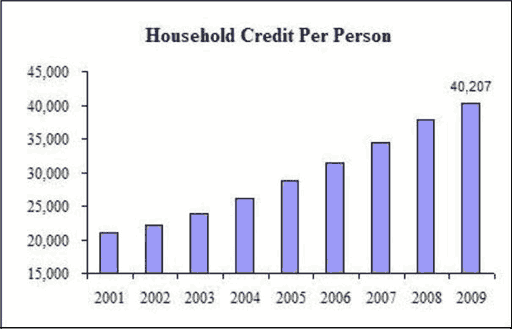

As the chart shows, back in the year 2000 we each had approximately $20,000 in debt, so in less than a decade the debt we are carrying has doubled. That’s a staggering statistic. If you are the average Canadian, your debt has doubled. Has your income doubled? Are you making twice as much today as you were earning in the year 2000? Probably not. If you still have a job you may have received “cost of living” increases of 2% per year for the last decade, but that obviously does not add up to a doubling of your income.

Canadians are extremely vulnerable, but do not seem to realize it:

Average Canadian household debt reaches $96,000The average Canadian family's household debt rose to $96,000 last year, a new study says. Debt-to-income levels rose to 145 per cent – the highest level ever recorded in the study, which has run annually for 11 years. The Vanier Institute of the Family study found a dramatic rise in late debt payments. Mortgage payments that were at least 90 days late were up 50 per cent over 2008.

Additionally, there was a rise of 40 per cent in credit card payments that were three months behind. The study said first-time mortgage buyers were taking on the most debt, unsurprisingly. However, the study says that many have taken advantage of record low interest rates and may have problems making payments if interest rates rise. Two-thirds of Canadians 18-34 would find themselves in trouble if their paycheque was delayed by only one week, a September 2009 survey by the Canadian Payroll Association found.

Canadians should also be looking south of the border, at the skyrocketing foreclosures in former bubble areas, despite a year-long rally in the credit markets. They should be looking at the inventory build-up that has already exceeded the crisis period of 2008, and continues to reach for the sky now that the credit markets have turned down again. Where the credit markets lead, the real economy will follow. If people cannot get financing, there will be no price support for real estate at anything like current housing prices.

Canadians should not be listening to MSM coverage of 'green shoots of recovery'. Those 'green shoots' are gangrene. The MSM, along with governments and central bankers, have been playing confidence tricks on the public for a long time. They are trying to convince people that there is nothing to worry about, that they should just go back to spending-in-their-sleep, as has become a well-entrenched habit.

Canadians need to wake up and look at the world around them - at where Ireland already is, and where much of the rest of Europe and the US are heading very quickly. To imagine that Canada can remain immune from tectonic shifts in the global economy is the height of folly. We are beginning to see some mention of Canadian housing bubbles, but the message is heavily downplayed by those who are prepared to mention it, and has not yet begun to sink in among the general population at all.

Housing prices due to fall, says think-tankCanada’s major metropolitan housing markets are looking awfully bubbly and are due to burst, says a report released Tuesday. The report, entitled Canada’s Housing Bubble: An Accident Waiting to Happen, by the Canadian Centre for Policy Alternatives, looks at prices in Toronto, Vancouver, Calgary, Edmonton, Montreal and Ottawa. It concludes that housing price appreciation is frothy in comparison to historic values.

“I think at best you will see stagnation in housing prices or some kind of correction, and at worst you will see the bubble bursting,” said David Macdonald, an economist and research associate at the centre.

Housing bubbles emerge when prices increase more rapidly than inflation, household incomes and economic growth. That has been the case for Canada over the last run-up in prices, according to the report.

Macdonald said this bubble is different than others, because for the first time it is spreading beyond Toronto and Vancouver.

“Canada is experiencing for the first time in 30 years a synchronized housing bubble across the six largest residential markets,” he said. [..] Macdonald gives three scenarios in which prices might drop.

- The first is similar to what happened in Vancouver in 1994, a market correction through price deflation. In that scenario, Toronto prices would decline by 9 per cent from an average of $420,000 to $382,000.

- In the second scenario, the bubble would burst more slowly, similar to the 1989 Toronto bubble. In that case, prices would decline by 21 per cent from $420,000 to $330,000 over a five-year period.

- In the worst scenario, a bubble would form similar to the United States and prices would fall rapidly. In that case Toronto prices would drop 20 per cent over three years to $335,000. The price drop would be slightly less than in scenario two, but happen more rapidly.

“Bringing house prices down just enough to moderate expectations but not so much as to cause a panic is a delicate balance,” says the report. “Government policy makers, the Bank of Canada, as well as rate setters at the big banks need to work together to steer the Canadian market to a soft landing. The alternative is not acceptable.”

Reality does not care what people find acceptable. Reality does not negotiate, it dictates. Real estate has further to fall here than almost anyone can image, as every bubble is followed by a substantial undershoot. Even as far as Ireland has fallen, or bubbly parts of the US, there is much further to go to approach pre-bubble prices, and the property crunch will take them much further than that. Canada has not even begun the extremely painful real estate deleveraging process. We have a very long way to fall indeed.

Beware those who think the worst is past

by Carmen Reinhart and Vincent Reinhart - Financial Times

The landscape of Jackson Hole, Wyoming, where central bankers gathered at their annual conference last week, is spectacular and forbidding. Jagged peaks and vast empty spaces stretch across the horizon. For the attendees, however, it was both a vista and a metaphor. Having lived through a precipitous global economic drop, they now must forecast how steep or flat will be the incline of recovery.

Ben Bernanke, chairman of the Federal Reserve, painted a sober but reassuring picture of US prospects. The basis for sustained recovery is in place, and canny Fed officials are now alive to the dangers of both deflation and inflation. Similarly Jean Claude Trichet, head of the European Central Bank, spoke about how the dust had begun to settle on the crisis. Policymakers and financial markets seem to be looking at what comes next.

Such optimism, however, may be premature. We have analysed data on numerous severe economic dislocations over the past three-quarters of a century; a record of misfortune including 15 severe post-second world war crises, the Great Depression and the 1973-74 oil shock. The result is a bracing warning that the future is likely to bring only hard choices.

Our research found real per capita gross domestic product growth tends to be much lower during the decade following crises. Unemployment rates are higher, with the most extreme increases in the most advanced economies that experienced a crisis. In 10 of the 15 episodes we studied, unemployment never fell back to its pre-crisis level, not in the following decade nor right up to the end of 2009.

It gets worse. Where house price data are available, 90 per cent of the observations over the decade after a crisis are below their level the year before the crisis. Median prices are 15 to 20 per cent lower too, with cumulative declines as large as 55 per cent. Credit is also a problem. It expands rapidly before crises, but post-crash the ratio of credit to GDP declines by an amount comparable to the pre-crisis surge. However, this deleveraging is often delayed and protracted.

Our review of the historical record, therefore, strongly supports the view that large destabilising economic events produce big changes in long-term indicators, well after the upheaval of the crisis. Up to now we have been traversing the tracks of prior crises. But if we continue as others have before, the need to deleverage will dampen employment and growth for some time to come.

Part of these changed prospects after a crisis simply reflects the correction of expectations. During episodes of financial euphoria – from the diving bell, through the steam engine and thereafter – the old rules seem not to apply. Lenders provide easy credit, investors bid up asset prices, and businesses invest unwisely. Spending advances rapidly, and debt builds up. Yet recent discussions about the “new normal” leave the misleading impression that the pre-crisis environment was “normal”.

Perceptions aside, at Jackson Hole, policymakers debated whether further measures to stimulate demand were needed. History shows that today’s problems could certainly materialise as a consequence of the failure to provide sufficient economic stimulus. In particular, a collapse in financial intermediation can reduce the availability of loans. This lack of access to credit, in turn, makes households and business less able to spend, lengthening and deepening the downturn. In such circumstances slow growth often becomes a self-fulfilling prophecy produced by timid authorities, who neither supported spending nor dealt with the capital-adequacy problems at large banks.

However, it is also possible that economic contraction and a slow recovery can dent aggregate supply, otherwise known as an economy’s ability to produce efficiently. In this scenario, much less discussed in current debates, a sustained stretch of below-trend investment, alongside the depreciation of human capital that comes from high unemployment, hits the level and growth rate of potential output. That is, the unemployment rate stays high because it has been high.

Importantly, this reduction in supply can also be caused by policy. In adverse economic circumstances, political leaders grasp for quick fixes that impair, not improve, the situation. The list of unfortunate interventions includes not recognising bank losses, as well as restricting trade (both domestically and internationally) and credit. In these cases the effects of crises might be persistent because we make them so.

A prudent post-crisis policy, therefore, must be alert to threats both to supply and demand, not demand alone. But the bigger worry remains the assumption that dust has begun to settle; that the shock from the crisis is temporary, when it is likely to be deep and persistent. Today, as in the past, over-optimistic fiscal authorities are over-estimating tax revenues. Financial supervisors want to believe that troubled banks are temporarily illiquid, not permanently insolvent. And central bankers like Mr Bernanke may soon attempt to restore employment to unattainably high levels. If they do so, the road to recovery will be long, and the lessons of history will have been ignored once more.

Carmen Reinhart is a professor at the University of Maryland and Vincent Reinhart is resident scholar at the American Enterprise Institute. This is based on a paper presented at the Jackson Hole Symposium.

White House: More Economic Stimulus Measures Coming

by Jared A. Favole - Dow Jones Newswires

President Barack Obama on Monday said his economic team is working to identify new measures to stimulate U.S. growth as part of a "full-scale attack" to strengthen the lackluster economy. Obama, speaking in the White House Rose Garden, said his economic team is "hard at work in identifying additional measures that could make a difference in both promoting growth and hiring in the short term, and increasing our economy's competitiveness in the long term."

It's unclear what new measures the Obama administration is considering, though Obama mentioned previously discussed proposals such as cutting taxes, extending financing to small businesses and boosting investments in renewable energy. White House Press Secretary Robert Gibbs declined to provide details about the new measures when pressed by reporters, but said Obama plans to lay out the new moves in the coming weeks. He said the new measures will take the form of targeted initiatives meant to spur growth and "create an environment where the private sector is not simply investing but also hiring."

The new measures, whatever form they may take, come as the Obama administration is facing greater scrutiny in the face of grim economic news. Last week, for instance, the federal government said the U.S. economy grew a sluggish 1.6% in the second quarter and corporate profits nearly froze. Obama said passing a small business bill that is stuck in the U.S. Senate will help. The legislation, which would provide tax cuts and boost lending to small businesses, is stuck in the Senate, blocked by Republicans. The Senate is currently on a summer recess until mid-September.

Obama urged Republicans to stop their efforts to block the bill, saying, "Holding this bill hostage is directly detrimental to our economic growth." Republicans have raised concerns that Democrats won't allow them to vote on individual amendments to the bill. Senate Republican Leader Mitch McConnell, of Kentucky, in a statement criticized the Obama administration's handling of the economy. "Instead of growing jobs as promised, Washington Democrats have grown the size of the national debt, the federal government and the unemployment rate," McConnell said.

Obama has said the small business bill would not add to the federal deficit but would be offset by other measures. He also criticized Obama for pledging to let tax cuts for wealthy Americans expire. McConnell said letting those tax cuts expire will hurt some small business owners. Gibbs said letting the tax cuts expire would only affect 3% of small business owners.

Obama also acknowledged that there is no "silver bullet that will reverse the damage done by the bubble-and-bust cycles that caused our economy into this slide." He added, "It's going to take a full-scale effort, a full-scale attack that not only helps in the short term, but builds a firmer foundation that makes our nation stronger for the long haul." Obama's comments came after he held his daily economic briefing with advisers, including Treasury Secretary Timothy Geithner, Council of Economic Advisers Chairman Christina Romer and economic adviser Larry Summers.

Japan renews QE as recovery falters

by Ambrose Evans-Pritchard - Telegraph

Japan has launched a fresh monetary and fiscal boost to shore up its faltering recovery and stem the slide into deflation, becoming the first major country to inject further stimulus since the Great Recession ended. The Bank of Japan agreed at an emergency meeting to boost its special loan facility by ¥10 trillion to ¥30 trillion (£220.7bn). "We need to watch out more carefully for downside risks to Japan's economy," said Governor Masaaki Shirakawa, who cut off his trip to the Jackson Hole forum in the US. "Several weak US figures came out, while the yen rose and stock prices fell. When we saw this, we decided that we need to take more precautions."

Premier Naoto Kan said Tokyo would tap into its reserve fund for a ¥920bn spending package on jobs and investment. "We want to take swift measures as the second pillar of stimulus to support easing by the bank," he said. The sums are tiny, a sign of Mr Kan's limited room for manoeuvre as public debt reaches 225pc of GDP. Rating agencies are already circling ominously. The economy stalled in the second quarter, growing just 0.1pc. Prices have fallen for the past 17 months. Core deflation is running at -1.1pc.

The Bank of Japan's move was too timid to stabilise exchange markets. The yen appreciated sharply to ¥84.6 against the dollar. It is once again closing in on a 15-year high. Julian Jessop, from Capital Economics, said the bank was responding "without enthusiasm" to political pressure to do something about the over-mighty yen. Mr Kan has been calling for "decisive action" to stem the yen's rise, now causing heartburn for exporters such as Toyota and Sony.

While the yen has at times been stronger against the dollar in real terms, it is the rate against China's yuan that worries Tokyo. This cross-rate is wildly out of kilter. Japan's curse is that the yen strengthens in times of crisis as investors repatriate money for safety. Life insurers and pension funds rotate from US bonds back into Japanese bonds as the yield gap narrows, which compounds Japan's deflation woes.

BNP Paribas said Japan may have more luck than Switzerland in driving down the currency if it chooses to intervene, since both monetary and fiscal policy are aligned in the same direction. Japan's authorities launched a huge purchase of US Treasuries during the deflation scare from 2003 to 2004 in order to weaken the yen. Mr Kan would like to see a repeat of such "shock and awe" action but has failed to convince Mr Shirakawa that the risks are worth it. Bank officials fear that a monetary blast might disturb a fragile equilibrium, bringing unwelcome attention on Japan's debts. Haunted by memories of Japan's hyperinflation, the bank is moving gingerly.

Even so, it is the first central bank to start loosening again. While the Bank of England has hinted at more quantitative easing, and the Fed is taking steps to avoid "passive tightening", neither has yet launched fresh QE.

Bank of England will use 'all powers' to stave off any future crisis

by Dominic Midgley - Telegraph

The deputy governor of the Bank of England signalled that the Bank would make aggressive use of new powers planned by the Government to head off any future financial crisis. In a major position paper, Charles Bean said that the Bank had been powerless to prevent what he called the "Great Contraction" of 2008 because control of interest rates was not, in itself, a powerful enough tool.

He also hinted that the days of quantitative easing may not be over: "The deleveraging process is incomplete, the recovery remains fragile and a considerable margin of spare capacity is yet to be worked off," he said. "Further policy action may yet be necessary to keep the recovery on track." He was speaking at the Jackson Hole Economic Policy Symposium in America the day after the Federal Reserve chairman, Ben Bernanke, buoyed the markets with an upbeat assessment of the US's growth prospects.

Mr Bernanke also hinted that he was prepared to employ more asset purchases if necessary. But Mr Bean devoted much of his speech to promoting the need to extend the range of the Bank of England's powers as part of the new "macro-prudential policy" – details of which will be revealed in the Financial Services Regulation Bill later this year. In his speech, Mr Bean gave examples of the sort of powers that could underpin such a policy. These included the right to force banks to build up extra reserves during boom times, increase risk-weights on high-risk lenders and impose loan-to-value ratios in the mortgage market.

"Monetary policy seems too weak an instrument reliably to moderate a credit/asset price boom without inflicting unacceptable collateral damage on activity," Mr Bean said. "Instead, with an additional objective of managing credit growth and asset prices in order to avoid financial instability, one really wants another instrument that acts more directly on the source of the problem. That is what 'macro-prudential policy' is supposed to achieve." His words received a cautious response from the British Bankers' Association.

"Charles Bean sets out some of the main tools the Bank might use to reduce risk in the economy, principally by increasing the amount of capital held against activities it considers too high-risk," said a spokesman. "This approach is already well-established in the UK and his speech helps to clarify how the Bank as chief regulator might use it in future." Mr Bean said he based his view that the Bank needed greater powers on research into the effect a sharp rise in interest rates would have had on the pre-credit crisis boom.

Increasing interest rates to 7pc from the end of 2004 to mid-2007 would, he said, have led to house prices a fifth lower at the end of 2006 and reduced the stock of real credit by 4pc. "This is trivial compared to the almost 50pc increase in the stock of credit seen over the period." He added that the new policy could only be implemented successfully if one body controlled all aspects of it.

A failure to unite the two regulators would lead to the creation of what he called a "push-me-pull-you" effect: "As he does not care about the capital gap directly, the monetary policy maker raises the policy rate [of interest] more aggressively in order to contain inflation. "And the macro-prudential policy maker, who cares primarily about the capital gap, moves to maintain bank capital by cutting the bank levy more aggressively."

In a list of the "multitude" of factors that contributed to the financial crisis, Mr Bean referred to "the moral hazard arising from financial institutions that are too big or too systemically important to fail, together with inadequate supervision of the same". He also included in his list "pay packages encouraging the pursuit of short-term returns", an obvious reference to bonuses.

The Unbearable Lightness of the Accounting Cover Up

by William K. Black - Benzinga

Bad bankers, bad regulators, and bad politicians love to cover up losses, fraud, and bank failures. The snake oil peddlers pushing for a cover up scream that if losses are recognized capitalism will collapse. Recognizing losses “causes” bank failures (ponder that “logic”). Bank failures cause other banks to fail. Selling bad assets of failed banks is invariably described as a “fire sale” that causes further falls in asset values, which causes more banks to fail, which causes more assets to be sold, which causes – the end of life as we know it.

If the snake oil guys are correct then financial markets aren’t fragile, they’re friable – a few bank failures away from crumbling. The solution under this logic is to lie about asset values and pretend that insolvent banks are healthy.

For a banker, what’s not to love about the right not to recognize even massive losses on assets? He gets to keep his job, reputation, and obtain bonuses for blowing up the bank. For a senior regulator whose failures allowed the bankers to cause the “epidemic” of mortgage fraud (FBI 2004), the mother of all bubbles, and the Great Recession a cover up is ideal. Bank failures are supposed to lead to investigations by the Inspector General and can lead to embarrassing congressional oversight hearings. Bankers and bad regulators sell the cover up to legislators as the miraculous “silver bullet” solution that can solve a crisis at no cost. Legislators wish everything they do could be that easy.

Among my most painful memories are being in their offices to listen to their explanation of how simple, cheap, and pleasant the cover up will be. Everyone wins, no one loses. It’s just like the financial bubble that inflated the fictional asset values. Remember how wonderful the bubble was? The cover up pretends that the bubble prices were real. The cover up strategy says that the answer to a bubble is a bigger, longer bubble. Fiction can be so much more pleasant than reality.

Fraudulent bankers are the biggest winners from the cover up. In addition to maintaining their jobs, reputation, and bonuses they dramatically reduce the risks of being prosecuted and sued. Bank failures are supposed to prompt investigations and severe sanctions against fraudulent and abusive managers. In the (vastly smaller) S&L debacle we obtained over 1000 felony convictions of senior insiders, over 1000 enforcement sanctions, and hundreds of successful civil suits. The S&L CEOs with the greatest political influence were frauds. They led the push to cover up S&L losses.

The cover up entered partisan politics during the 2008 presidential campaign. Senator McCain’s first big speech on the developing crisis called for changing the accounting rules to prevent loss recognition. Bill Isaac (former FDIC Chair – and leader of the cover up of bank losses during the LDC debt crisis) was invited by the Republican and “Blue Dogs” (conservative Democrats) caucuses considering the first TARP bill to brief them on how to respond to the crisis. He opposed passage, assuring them that if they changed the accounting rules to hide the bank losses they would prevent $500 billion to $1 trillion in losses.

This emboldened the Republicans and Blue Dogs to unite and defeat the first TARP bill. McCain had announced that he was suspending his campaign and returning to the Senate to secure passage of the TARP bill. McCain was poorly positioned to counter Isaac’s arguments because McCain had proposed the same accounting gimmicks Isaac was proposing. The defeat of TARP I embarrassed McCain and Senator Obama’s lead over Senator McCain in the polls increased substantially.

Senator Obama, as a candidate, and his administration after the election did not take a public position on covering up the losses. The Chamber of Commerce and bank lobbyists made the cover up of bank losses their top regulatory goal. Their strategy was to get Congress to extort the Financial Accounting Standards Board (FASB) to force a change in the accounting rules so that banks did not have to recognize loan losses.

House Financial Services Capital Markets Subcommittee Chairman Paul Kanjorski (D., Pa.) held a hearing in March 2008. The hearing was a bipartisan assault on FASB. Kanjorski demanded the prompt adoption of the cover up. Otherwise, he promised the prompt passage of legislation to remove the FASB’s power to se accounting rules. The Chamber, of course, is a fierce opponent of the Obama administration. Nevertheless, the administration took no action to counter the Chamber’s unprincipled attack on accounting principles.

Bernanke gave open approval to the Chamber’s efforts to cover up bank losses. The Obama administration took the exceptional step of nominating Bernanke, a conservative anti-regulatory Republican, for an additional term as Fed Chairman. The administration found the cover up useful to its campaign to use stress tests to restore confidence in the banking system. If the banks had been required to recognize their losses the stress tests would have shown that many of the largest banks were insolvent or on the verge of insolvency. The stress tests were shams based on fictional, grossly inflated asset values. Cover ups make for strange bedfellows.

Congress enacted the Prompt Corrective Action (PCA) law in 1991. PCA was adopted because the cover up of S&L and bank losses in the 1980s increased losses severely and left bad and even fraudulent CEOs in charge of federally insured depositories. The PCA was based on theoretical work by conservative economists who feared regulators’ perverse incentives to allow banks to cover up losses, but it attracted broad bipartisan support. Its purpose was to constrain regulatory discretion and mandate the prompt correction or closure of failing and failed banks. As we warned its proponents in 1991, however, it had a critical gap that could be exploited to undermine the statutory goal.

The PCA is triggered primarily by inadequate capital. Banks fail primarily because they invest in assets whose values fall sharply. Capital is an accounting concept. When a bank overstates its asset values its reported capital is inflated. The PCA was prompted by accounting cover ups of asset losses – but it can be eviscerated by accounting cover ups of asset losses. The Bush and Obama administrations exploited this loophole by refusing to crack down on many enormous banks that grossly inflated their asset values and reported capital.

Instead of holding oversight hearings that exposed the Bush and Obama administrations’ evasion of the PCA and demanded compliance, prominent members of Congress encouraged it. House Financial Services Chairman Barney Frank (D., Ma.) said: "This is important for all regulators. We need to give you some discretion in how you react to these things. I am asking everyone -- the Office of the Comptroller of the Currency and others -- if anything in the existing legislation deprives you of discretion in how you react ... I insist that you tell us."

Congress passed PCA to remove the regulators’ discretion to cover up or ignore bank losses. Now, the key House Chair – who once rightly criticized the S&L regulators for not promptly closing insolvent S&Ls – encourages the regulators to employ discretion to cover up or ignore bank losses.

Why the Fed's Hands are Tied When it Comes to Deflation

by Susan C. Walker - Elliott Wave International

With consumer prices rising so little that they look like a deflating soufflé, Fed Chairman Ben Bernanke now has publicly faced the fact that the Fed must fight deflation rather than the central bank's old nemesis, inflation. At a meeting in Jackson Hole, Wyo., this week, he said what he had to say -- that deflation is "not a significant risk for the United States at this time." Nonetheless, in time-honored Fed speak, he added that the Federal Reserve "will strongly resist deviations from price stability in the downward direction.”

As the New York Times reporter commented in the August 27, 2010, report, "It was his most robust statement to date that the Fed would do its part to avoid a Japanese-style deflation from taking hold."

Watch out, below! Here comes more quantitative easing, which means that the Fed will create more money on its books and start buying up banks' bad loans to provide them with more money to lend. But the Fed can only go so far with this policy, as Bob Prechter explains in an interview he did with Justin Brill, managing editor of The Daily Crux, a financial daily digest website.

* * * * *

Excerpted from a transcript of the interview, which appeared in the June 2010 edition of The Elliott Wave Theorist , by Robert Prechter

The Daily Crux: But, ultimately can’t the Fed simply “print” money if it appears deflation is starting to win? The “drop money from helicopters” analogy you mentioned earlier? Wouldn’t that prevent outright deflation and ultimately lead to inflation or even hyperinflation as the dollar is devalued?

Robert Prechter: To begin with, the printing analogy is flawed. The Fed does not operate a press, as the government of Zimbabwe did. It creates new money only when it buys IOUs. This may seem to be a distinction without a difference, but it’s actually very important. These IOUs are the Fed’s assets, and it doesn’t want worthless assets backing its notes.

Even if the Fed were to monetize every dime of currently outstanding, dollar-denominated debt, it would create no net inflation. The money-plus-credit supply would be the same. And price levels — especially for investments — are based on the total of monetary assets, not just base money. Even so, there is no way that the Fed will buy up the entire world’s stock of lousy IOUs. It has always wanted pristine assets on its books. Remember, it didn’t buy Fannie and Freddie’s IOUs until it got the Treasury to guarantee them.

Then there is the so-called moral hazard — not that the Fed cares about morality — meaning that if the Fed were to begin buying everyone’s IOUs, people would immediately issue more IOUs as fast as they could and sell them to the Fed. It couldn’t keep up with the volume. But these scenarios are fantasies. In reality, self-preservation will eventually motivate the Fed just as it motivates every other institution. Buying too many worthless assets would cause the Fed’s self-destruction, and I think it will balk at going that far.

The Daily Crux: OK, so you don’t think the Fed will go that far. But what if the government got involved and tried to inflate its way out by issuing massive amounts of Treasury bonds to the Fed? Wouldn’t that create inflation?

Robert Prechter: If the government tried to do that, bond holders would get spooked, and interest rates would go up and stay ahead of the printing. At the same time, other credit prices — municipal, corporate and consumer — would implode. When the supply of credit is far bigger than the supply of money — and it is by a huge margin — the value of old credit can contract faster than new bonds can be printed. The net result would still be deflation.

But this is not the most likely scenario. Have you noticed that even the Fed chairman has been telling Congress it needs to stop spending and borrowing? The Fed doesn’t want this to happen any more than other creditors do.

If the Treasury’s interest rates do soar, it will not likely be due to inflation fears but to fear of government default. If the government is forced to pay higher and higher rates, it will become a black hole for money. Spiraling Treasury rates would suck money from other sources, causing banks, municipalities and companies to fail, ruining all of their debts, which would be deflationary.

China's rising bank debt could leave nation exposed

by Ambrose Evans-Pritchard - Telegraph

Moody's rating agency is concerned that China is powering its economic growth by raising the gearing of the banking system, leaving the country exposed if the outlook darkens. The banks are expanding their balance sheets rapidly through higher leverage – a policy that relies entirely on the continuance of torrid growth. "Pain lies ahead if China's economic growth slows and the banking business model cannot adjust accordingly in time," said Yvonne Zhang, the agency's senior China analyst.

Moody's said China Investment Corporation (CIC), the country's sovereign wealth fund, borrowed $8bn (£5.1bn) last week to recapitalise three state-owned banks, using debt rather than genuine equity to boost bank capital. The agency said that beefing up the banks by this method is "credit negative" for China as a whole: "The increases in assets and equity are artificial and without real economic substance. The increase in reported equity enables the banks to lend more and effectively leverages up the system."

The agency does not explore why the CIC is resorting to debt to carry out these transactions, but the practice looks bizarre from the outside and prompts questions over the resources of the fund itself. Concerns are mounting about the opaque operations of China's banks. The regulator ordered them to carry out a stress test this month based on a 60pc fall in property prices. It is probing $1 trillion of local government loans at risk of impairment.

US housing woes compound job fears

by James Politi - Financial Times

Concerns that the depressed US housing sector will remain a drag on the US labour market have mounted following the loss of nearly 120,000 jobs in construction and related businesses in the last three months for which statistics were available. According to Financial Times analysis, the decline in housing-related employment was the biggest weight on private sector job creation as it slowed to an average of 51,000 jobs a month during the May-July period from 153,000 a month in February-April.

US Labor Department data show that some 61,000 construction jobs were lost between May and July, with another 56,000 positions shed in ancillary areas, such as furniture, building products and financial services related to property. New employment data for August will be released on Friday, and economists expect little improvement in the current anaemic rate of private sector job creation, which is not enough to bring the unemployment rate down.

“The fact is that too many businesses are still struggling, too many Americans are still looking for work, and too many communities are far from being whole again,’’ President Barack Obama said on Monday as he revealed that his advisers were considering further tax cuts designed to encourage job creation.

Construction and associated businesses were among the hardest hit sectors in the recession, accounting for about 3m of 6.6m jobs lost after the collapse of the housing bubble in 2006. The manufacturing sector lost more than 2m jobs in the same period, but appears to be emerging from the downturn in a healthier state. Manufacturing added 88,000 jobs between May and July, and 73,000 positions between February and April.

Construction and related industries added some 18,000 workers to their payrolls in the February-April period. The return of significant job losses in these sectors will increase worries among economists and policymakers of a further jump in long-term unemployment, as many of these workers struggle to find jobs in different industries or locations. Construction’s contribution to overall US employment – measured by private non-farm payrolls – was about 6 per cent between 1980 and the early part of this decade, peaking at 6.7 per cent in October 2006. Construction now accounts for just 5.1 per cent of private sector jobs.

The Answer To A Housing Recovery: Lower Prices

by The Pragmatic Capitalist

The simple economics behind the situation in housing is beginning to become more apparent as the weeks go by. As we’ve noted for several years now the primary problem in the US housing market remains one of supply and demand. As the jobs market continues to weaken, deflation takes hold of the US economy and the shadow inventory floods the market the math here remains simple enough for an Econ 101 student to understand. In order for the housing market to build a firm foundation that does not require government aid we will need to see a reduction in prices. In a recent research report Merrill Lynch described just how extreme the supply/demand imbalance has become in recent months and years:“The collapse in housing demand means that it likely will take even longer to clear the inventory of homes for sale. In the new market, builders have continued to slash construction, maintaining incredibly lean inventories, and yet there is still supply of 9.1 months. Even more worrisome, however, is the existing home market where inventory is still on a decisive uptrend. As such, it takes 12.5 months to clear the inventory at the July sales pace. This widening gap between housing demand and supply means that construction likely will remain depressed and prices will dip lower (Chart 5).”

More worrisome is the huge increase in shadow inventory that Merrill expects:

“The inventory of existing homes for sale is set to increase further as “shadow inventory” moves into the market. According to the latest Mortgage Bankers Association’s report, 9.1% of loans outstanding, which translates to 4.8 million, were seriously delinquent at the end of Q2 (capturing 90+ days delinquent or in the process of foreclosure). Unfortunately, this is not the end of the foreclosure pipeline. There were 2.6 million of mortgages either 30 or 60 days delinquent (Chart 6). It is likely that re-defaults from failed modifications – there have been 616,839 failed HAMP modifications – have contributed to early stage delinquencies.”

Based on Merrill’s estimates the housing market is unlikely to normalize before 2015. The supply/demand imbalance is simply staggering at the current levels and is likely to deteriorate if the economy weakens further:

“We define a normal housing market to be one in which housing starts are trending at the historical average of 1.5 million homes a year. In our view, we are several years away from this state of normalcy. Housing supply has outpaced housing demand by about 2 million homes over the past few years and is on pace to add another 500,000 excess homes by the end of 2012. For this excess to clear, housing starts must remain at a depressed level, not returning to normal until 2015. This would make it the slowest housing recovery in post-war history.

If we pencil in our baseline forecast for housing starts of 590,000 this year and 690,000 next year, another 500,000 excess homes will be created. Looking ahead, we must be more judgmental. A reasonable scenario is that starts slowly edge higher to 1 mn by 2013 and reach the “normal pace” of 1.5 mn by 2015. At this point, most of the excess supply will have nearly cleared, allowing starts to pick up to match the pace of demand.”

Congress is currently discussing creative new ways to prop up this market. It should be plain as day at this juncture that the government cannot fix the housing market with their incessant fidgeting. The market needs to correct further before reaching a sustainable bottom. Lower prices will act as an automatic stabilizer by generating significant demand. At this point, more government intervention merely kicks the can down the road by pulling demand from the future. We can continue to deny the simple economics at work here, but at some point the market will prevail and prices will settle at a level that the market can absorb. In my opinion, the sooner this happens the sooner we can get on with the recovery process. Unfortunately, politicians have elections to win so they will continue to use their law degrees to attempt to change the laws of economics. It won’t work.

5 reasons why falling home prices will be good for the economy

by Doctor Housing Bubble

A recent report shows that 11 million homeowners with a mortgage are underwater with a deep red line item on their household budget. Add into the mix those with less than 5 percent equity and we realize that 28 percent of all “homeowners” are either in a negative equity position or teetering close to it. States like California have negative equity rates of 33 percent thanks to the growth of highly questionable mortgage products. Yet California looks like a saint when compared to Nevada with an underwater rate of 68 percent!

If we want to examine the core premise of the debate surrounding the bailouts, it is that higher home values by default are good for the economy. I would argue that having high home values as a mission is misguided if that is the only goal we are seeking (and that is basically what we have been doing for the last few years). In fact, the majority of Americans would benefit from lower home prices. A market with higher home values is only beneficial if incomes and the economy move along in synchronization. Popping the last few balloons of the housing bubble is a good thing for most. Let us examine five reasons why falling home prices will be a good thing for the economy moving forward.

Reason #1 – As real estate values inflated actual owners’ equity plummeted

The above chart is of paramount importance in understanding the housing bubble. For fifty solid years, homeowners had at least 50 percent equity in their homes nationwide. It is fascinating that during the biggest jump in housing values that actual equity collapsed. What happened? Low to nothing down toxic mortgages funneled by Wall Street and the invention of the home equity ATM. If we slice the above chart into a smaller timeframe and only look at the last decade, we see this insidious trend:

This chart pinpoints the last decade of growth for our economy. To sum up what happened, as the middle class struggled to gain any advantage in actual wages the home became the one-stop shop for consumer spending. Why save $500 a month when you can yank out that much money from your home equity and keep spending going? Of course the problem with this is that it is unsupportable and now the taxpayer is footing the bill. But as we will show later, the burden of the recession has fallen disproportionately on the shoulders of the working and middle class while banks have shielded themselves from the worst parts of the recession.

Why the recent increase in homeowners’ equity? This is good news right? Not exactly. The recent bump that you see is due to people losing their homes through foreclosure. For example, say a subprime borrower bought a home in an area with low incomes for $400,000. The home is now valued at $200,000. If the borrower is current, this is a drag of $200,000 on the equity chart. After foreclosure, a figure of zero actually helps the bigger mortgage pie. So expect this figure to increase in the short-term as foreclosures remain elevated.

Reason#2 – Real estate should not be the primary driver of the economy

Financial sector profits are back to near record levels:

Source: Gluskin Sheff

It is interesting to note that back in the 1950s when Americans had their highest levels of owners’ equity, the financial sector was less than 10 percent of all total corporate profits. Today, it is back up reaching nearly 30 percent. Real estate and the financial sector is now a drag on the overall economy. Finance and capital allocation should be on creating and producing real value in the real economy. Today with no actual changes to Wall Street, we have days with flash crashes that erase trillions of dollars in wealth for most but actually make billions for a select handful of banks. The profit is now in speculating on the biggest casino on Earth. For the last decade, real estate was the hub of this speculation. Today, it is a matter of chasing the latest algorithm and trying to beat other hedge funds to the latest calculation that can rob wealth from the real economy.

If you look at the above chart, we seemed to do well with bread and butter 30 year fixed rate mortgages. For the large part of 50 years we required people to put down 20 percent to purchase a home. That seemed to work and actually provided the biggest net worth boost to individual households and ushered in the largest middle class the world has ever seen. The latest gimmicks and mortgages seem to be only helping one tiny sector of the economy.

Any time you allow easy access to debt, expect to see massive inflation in prices. We have seen this with the auto industry, college tuition, and with of course housing. When you give people the ability to borrow whatever they like, many will do it. Some will argue that this is a question of personal responsibility. I agree. But the propaganda that banks won’t tell you is that they are gambling with taxpayer money. If banks wanted to lend someone $20,000 a year with no income so they can go to a paper mill institution, so be it if the money comes from their capital pool. But the money is largely taxpayer backed. They are funneling taxpayer backed loans into this market so care not if the loan defaults. The magicians of our time are the banks.

Reason #3 – The brunt of the recession has been shouldered by households

The above chart highlights the inequality in the bailouts. The biggest line item for household net worth is residential real estate values. Households in the U.S. have lost over $6 trillion in real estate values since the bubble popped. Interestingly enough, mortgage debt has only fallen by $372 billion. Banks are able to suspend reality and avoid using mark to market accounting so they can continue to gamble on Wall Street. Most typical American families have to contend with actual market values. The massive amount of toxic mortgages still out there is astounding yet banks continue to pretend that things are fine. What this does is stunts the actual clearing ability of the market. Japanese banks did this for decades and how did that turn out?

Home values are going down because Americans are now dealing with more normal market factors. We are now looking at incomes (at least at a more modest level) and as it turns out, the economy is not healthy. We are now looking at debt through a microscope and as it turns out, many households are maxed out. So lower home values are good for those looking to buy. The only way home values can remain high is if the government and Wall Street keep pretending that bubble values actually had some fundamental reason to be so high. Ironically agencies like the FHA which have a core mission to help fund affordable housing are actually the main tool in the market today keeping home prices inflated. I mean how can this agency say they stand for affordable housing when they are backing loans up to $729,250 in value?

Reason #4 – Not everyone benefits from a housing bubble

The brutal reality is that falling home values will actually help many out in the current market:

If you combine those who are renters and those who have zero mortgage debt, these two groups would make up the majority of households in the U.S. Renters will definitely benefit because they can purchase homes at a lower price without going into incredible amounts of debt. Instead of blowing a large part of their income on the mortgage, they can use freed up disposable income to actually spend in the real economy. Who wins when someone is funneling 50, 60, or even 70 percent of their income into a home?

Those who have paid off their house win either way. If home prices fall, they will get less for their home but at the same time, other home prices will fall so they can purchase a home at an adjusted level. Many of these people are not looking to move so either way it is a moot point. The only people that are obsessed with home values are those who are now real estate speculators.

28 percent of households with a mortgage are either underwater or near negative equity. It is hard to call this group homeowners. For many, the only way out is for home values to surge. Yet many jumped in with low down payment mortgages so they have a big incentive to walk away. With a glut of rental housing, many would win simply by walking away, fixing their credit, and buying a home in a few years if they are able to meet stricter lending requirements (we can hope this plays out for the sake of our economy). If you think about it, the only big loser here is the banks holding the mortgages. Now you understand why the entire focus of the bailouts has been on banks. Strip the layers of the onion back and follow the stinking money.

Reason #5 – Negative equity is a drag on the economy

Source: Calculated Risk

Many of those with negative equity are already walking away from their homes. They made a bet and lost. The only way banks can combat this behavior is ignoring missed housing payments and allowing people to stay in the homes while they keep mortgage debt on their balance sheets at inflated levels. But the longer this game of pretend goes on, the worse it is for the economy. Right now the vast majority, renters, those with paid off homes, and homeowners with equity who pay on time are watching this game between negative equity homeowners and Wall Street play out. Why should the majority be brought down because of the bad bets from these two groups? Realize the losses and move on. Otherwise, more and more taxpayer money from the other groups will be shifted to this area. That is not good.

In the last few weeks after I tossed out an estimate of nationwide home values falling by 25 percent, a handful of articles made the rounds predicting a similar figure. This was not some doom prediction for housing but will actually help the overall economy realize the losses and move on. In therapy, you have to accept a mistake to move on. At times, this realization will be painful but in the end it is better for you. Right now Wall Street is in complete denial and trying to pretend all is well. Their profits are up but all that is happening is a wealth transfer from taxpayers to this unproductive group. Lower real estate values will be better for the economy moving forward until wages catch up. If wages don’t catch up why should we insist on keeping prices inflated? Who really wins with higher home prices?

House prices have nowhere to go but down

by Larry Elliott - The Guardian

With first-time buyers unable to get on the ladder, the property market is shuddering to a halt

Only a mug bets against rising house prices in Britain. This is a small island that has a rising population, tight planning controls and a tax system that favours property. Demand tends to run well ahead of supply, and that means bricks and mortar always seems a good investment.

Well, call me a mug if you like, but house prices are overpriced and have to fall. Activity is weak, with the number of new mortgage applications running at less than half their pre-recession levels. First-time buyers, according to a survey from Rightmove out today, account for only 20% of the market, about half the level needed to lubricate housing chains. A separate snapshot of the market from Hometrack says that sagging prices are more than the customary seasonal lull.

On the face of it, this seems strange. Friday's revised figures for UK growth in the second quarter showed output expanded by 1.2% – the strongest surge in nine years. Traditionally, there is a symbiotic relationship between growth and house prices; the two feed off each other. At the moment, however, this relationship has broken down and it's not hard to see why: the market has been rigged in favour of existing owner-occupiers at the expense of those trying to get on the housing ladder. Bank rate was cut from 5% to 0.5%. The Bank of England launched its quantitative easing programme, which has added £200bn to the money supply. Ministers put pressure on lenders to go easy on those in mortgage arrears.

All this was done with the best of intentions. Back in the early 1990s, Britain saw record repossessions when boom turned to bust. Given that the downturn of 2008-09 was far more severe, there were justifiable fears that a tidal wave of repossessions would tip Britain into a full-scale slump. The policy was a double success. First, repossessions were capped at about half the levels in the milder recession two decades earlier. Second, the boost to real incomes for those with variable-rate home loans meant that they could spend a bit more while at the same time paying down their debts.

But there was a downside to rigging the market in this way: it created what economists call a classic insider-outside problem. When the property bubble popped in the late 1980s, house prices fell for six years, making them affordable again for first-time buyers. This time, the scale of the policy response meant prices steadied much more quickly; they were edging up in the spring of 2009, even though economic output was still falling.

Heck of a squeeze

The much more cautious approach adopted by lenders made matters worse. In the boom years, the easy availability of 100% home loans meant many first-time buyers could pay inflated prices, even if it was one heck of a financial squeeze. But once the credit crunch arrived, banks and building societies started to ask for deposits of 20% or more. The average price of a home is well over £150,000, putting property out of the reach of all but the wealthiest first-time buyers.

Only three things can happen in these circumstances. The incomes of potential first-time buyers can rise so that they can afford higher prices. House prices can fall to make them compatible with what first-time buyers can currently manage. Or – and this best sums up the present position – the property market comes to a grinding halt.

Miles Shipside of Rightmove said: "Many of those who should be buying for the first time have declared themselves as non-participants in the housing game. Due to the new deposit rules they have to play by, it comes as no surprise that they are staying away, as they are probably busy saving." The Council of Mortgage Lenders says the number of first-time buyers is down from 500,000 a year at the turn of the century to 200,000.

Governments have sought to address the problem by cutting stamp duty for first-time buyers but the reduction has not been nearly enough to counter what is a deep, structural flaw in the market. Work by Professor Steve Wilcox at the University of York's Centre for Housing Policy showed that in 40 local authority areas back in 2005, 40% of younger working households – the key first-time buyer demographic – were earning enough to pay more than a social sector rent but not enough to buy even the cheapest available home.

The Chartered Institute of Housing (CIH) has a name for this group – the "in-betweens", caught in a twilight zone between housing dependency and fending for themselves. These are precisely the families lionised endlessly by politicians of all colours: the hard-working people who play by the rules, are ambitious to get on, and want to fend for themselves. Hard-working families may be idealised on the hustings but, as Sarah Webb, the CIH chief executive, rightly notes, "they are forgotten when it comes to their housing needs and aspirations".

A century ago only 10% of Britons owned their own homes. The proportion rose steadily in the three decades after the second world war but by the start of the 1980s, about 45% of people still rented their homes from the private or public sector.

The UK then embarked on what market participants call the golden age of owner-occupation. In the first wave during the 1980s, right-to-buy legislation and financial deregulation gave families in council homes the opportunity to buy property at bargain prices. The housing downturn of the early 1990s was then followed by a second wave stimulated by a long period of low inflation, rising employment and cheap money. According to the CIH, this golden age is now over, a conclusion backed up by figures that show owner-occupation in England peaked at 71% in 2002-03 and had fallen to 68% by 2008-09, the year the financial crisis was at its most intense.

Baby boomers

There has been much talk recently of the sins of the baby boomers, and when it comes to the property market there is a case to answer. Rising prices have been great for the older age groups, particularly those seeking to trade down on retirement, but bad for potential new entrants to the market. They either have to rent, live at home for longer, or hope that their parents will use some of their windfall gains from the property market to pay the deposits on their children's first homes. This, of course, is an option open only to the winners from the system, which tends to mean the better off in the better-off parts of Britain. The upshot is housing inequality every bit as pronounced as income inequality.

So what can be done? Ministers could give councils and other providers the right to build more homes in the parts of the country where people want to live. A combination of nimby-ism and spending cuts makes that unlikely. They could promote an active regional policy that might encourage people to move to those parts of the country oversupplied with homes. Given that the spending cuts are likely to fall heaviest on the regions outside of the south-east, that too looks improbable.

They could, of course, be bolder over tax, imposing a land value tax instead of putting up VAT, an idea backed by Andy Burnham, one of the contenders for the Labour leadership. But that, in property-fixated Britain, is for the birds. Despite the policy inertia, the market will eventually adjust to the underlying reality. A lack of first-time buyers equals weak activity equals lower prices. It may be a long, drawn-out process.

Canadian housing prices due to fall, says think-tank

by Tony Wong - Toronto Star

Canada’s major metropolitan housing markets are looking awfully bubbly and are due to burst, says a report released Tuesday. The report, entitled Canada’s Housing Bubble: An Accident Waiting to Happen, by the Canadian Centre for Policy Alternatives, looks at prices in Toronto, Vancouver, Calgary, Edmonton, Montreal and Ottawa. It concludes that housing price appreciation is frothy in comparison to historic values.

“I think at best you will see stagnation in housing prices or some kind of correction, and at worst you will see the bubble bursting,” said David Macdonald, an economist and research associate at the centre. Housing bubbles emerge when prices increase more rapidly than inflation, household incomes and economic growth. That has been the case for Canada over the last run-up in prices, according to the report. Macdonald said this bubble is different than others, because for the first time it is spreading beyond Toronto and Vancouver. “Canada is experiencing for the first time in 30 years a synchronized housing bubble across the six largest residential markets,” he said.

Major banks have reached conclusions similar to those of the left-of-centre think tank. The Toronto Dominion Bank has estimated that average prices are 10 to 15 per cent too high, while the CIBC has said prices are 14 per cent overvalued. Canada has only had three bubbles. Toronto experienced a large bubble in 1989, while Vancouver had two burst in 1981 and 1994. Macdonald said a full-blown crash can still be avoided if mortgage rates do not ratchet up quickly and if government puts more stringent requirements on lending.

He said legislation could be introduced to return mortgage lending to 2006 criteria, where purchasers had to put 10 per cent down for a 25-year amortization. Although the federal government already put tighter restrictions in place earlier this year, buyers still have the option of putting 5 per cent down and can take a 35-year amortization on homes. “Consumers should also play a part by not buying more house than they can afford,” says Macdonald.

The report says the last bubbles were triggered by interest rates moving up by just one per cent above the two-year rolling average. “It doesn’t take much for consumers to take pause, especially those who are used to seeing such low rates,” said Macdonald. “You also have a lot of consumers, particularly outside Toronto and Vancouver, who have no memory of what a bubble is like or the aftermath.”

Low mortgage rates, access to easy credit and net immigration have also contributed to price pressures, said Macdonald. Between 1980 to 2000, the historical price range for housing stood at between $50,000 and $80,000 in inflation-adjusted 1980 dollars. But within a brief five-year period from 2001 to 2006, major housing markets shot to well above that $80,000 average, according to the report. “The comfort level isn’t there as affordability erodes,” said Macdonald. Housing prices have stayed in a narrow range of 3 to 4 times income in the 20 years before 2000. The problem is, says Macdonald, is that housing prices adjusted for income today are anywhere from 4.7 to 11.3 times annual income in the six major areas.

Not everyone agrees with the findings of the report. Toronto economist Will Dunning says that the market cycle is in a cyclical downturn – not a bubble. “It is quite possible that the next phase of the cycle will be a partial reversal of the price gains of maybe 5 to 10 per cent, but this is not a post bubble collapse,” says Dunning. “It is the operation of a functioning market in which the vast majority of buyers are making decisions based on their real needs, not the mindset normally associated with bubbles.”

Despite their differences, all analysts seem to agree that prices could fall. Macdonald gives three scenarios in which prices might drop. The first is similar to what happened in Vancouver in 1994, a market correction through price deflation. In that scenario, Toronto prices would decline by 9 per cent from an average of $420,000 to $382,000. In the second scenario, the bubble would burst more slowly, similar to the 1989 Toronto bubble. In that case, prices would decline by 21 per cent from $420,000 to $330,000 over a five-year period.

In the worst scenario, a bubble would form similar to the United States and prices would fall rapidly. In that case Toronto prices would drop 20 per cent over three years to $335,000. The price drop would be slightly less than in scenario two, but happen more rapidly. “Bringing house prices down just enough to moderate expectations but not so much as to cause a panic is a delicate balance,” says the report. “Government policy makers, the Bank of Canada, as well as rate setters at the big banks need to work together to steer the Canadian market to a soft landing. The alternative is not acceptable.”

Need for big deposit hits UK home sales hard

by Philip Aldrick - Telegraph

The housing market is under threat from a shortage of first-time buyers as they are priced off the property ladder by the large deposits needed, new research shows. Just one in five prospective buyers is making a first purchase, the lowest on record and half the level needed for a stable housing market, according to property website Rightmove. Without a ready supply of new buyers underpinning transactions, property chains may collapse, pulling down prices all the way to the top.

Miles Shipside, director of Rightmove, said: "With the number of prospective buyers at the bottom of the chain being half normal levels, the question sellers further up the chain will be asking is, 'Who will be at the bottom of my chain?'" He added that banks are demanding larger deposits, making mortgages less accessible to first-timers. Mr Shipside said: "Due to the new deposit rules they have to play by, it comes as no surprise that they are staying away as they are probably busy saving."

First-time-buyers need on average a 25pc deposit now compared with 10pc before the financial crisis. Data from the Council of Mortgage Lenders shows that 80pc of first-time-buyers under 30 need assistance from parents, and that the average age of an unassisted first-time-buyer has risen from 33 to 37 in the past five years. Most economists now forecast house prices to fall in real terms, once adjusted for inflation, for several year

Mortgage brokers are becoming a vanishing breed

by Jeff Swiatek - The Indianapolis Star

Most of the mortgage brokers that seemed to populate every office building and commercial street in cities nationwide just five years ago have vanished. Ken Blaudow, owner of Indy Mortgage had 85 employees originating home loans in 2003. Now he has three and is about to give up his leased office in Castleton, Ind., and move his company into two bedrooms of his house. "It's drastically down," he said of his industry. "And there are a lot of funky new rules."

Much of the decline has come from the implosion of the housing sector since 2007. Prices and sales plunged during the recession. Foreclosures hit record highs almost everywhere. As government rushed in to respond to the crisis, caused in part by overselling of risky mortgages by brokers who got rich on exorbitant fees, regulations on the industry multiplied. States in the past two years began requiring brokers to pass licensing exams and undergo background checks. A criminal record, even a past bankruptcy, can now prevent someone from writing a mortgage. If states don't already do it, a federal law coming in January will require licensing exams and criminal background checks nationally.

Brokers and loan originators find lenders for people seeking a mortgage on a new home purchase and charge a fee for that service. Many of the sometimes-exotic products that independent brokers used to push — jumbo loans, subprime mortgages — also have been restricted or banned. The new industry that's emerging is much more conservative, regulated and, some would say, less consumer-friendly. "I don't think (the changes) will be better for the industry. It costs more to do business. And the consumer has fewer choices. But those are the cards we have been dealt," said Al Thorup, executive director of the Indiana Mortgage Bankers Association.

A study by Bankrate, a financial information supplier, found that mortgage fees are on the rise, jumping 23% in the past year alone. Nationally, the average fees that a homeowner paid for a $200,000 loan are $3,741, compared with $2,739 last year. This does not include fees for real estate agents typically paid by the seller. Bankrate says the jump in mortgage fees is due in large part to the increased scrutiny lenders must give every loan, under tougher guidelines from federal regulators and two quasi-government companies that guarantee loans, Freddie Mac and Fannie Mae. "It takes five to six times the work to get a loan to close than it did two years ago," Blaudow said.

Credit histories must be dutifully compiled for all borrowers. And any number of new criteria can lead to a refusal to lend. One new practice closes the door on loans to anyone who's done a short sale — a way of selling a house when the sale proceeds fall below the balance on the mortgage — in the past three years.

Banks have actually fared well in the restructuring of the mortgage industry. That's because many banks didn't engage in the riskier lending practices, such as granting adjustable loans at subprime rates to people with less-than-stellar credit, that some independent brokers and their companies did. Banks also will be better able to bear a coming federal regulation that will require any company handling federal FHA or VA loans to have $2.5 million in assets.

Ron McGuire, president of F.C. Tucker Mortgage in Indianapolis, said the changes in the mortgage industry mean "we're back to the way underwriting was 20 years ago when you had to have a down payment, you had to have a job. And that's a good thing." But McGuire said he worries that the decline of independent brokers now gives a handful of large national banks more of a chance to dominate the mortgage industry.

Why Cheaper Money Won't Mean More Jobs

by Robert Reich

Can the Fed rescue the economy by making money even cheaper than it already is? A debate is being played out in the Fed about whether it should return to so-called “quantitative easing” – buying more mortgage-backed securities, Treasury bills, and other bonds - in order to lower the cost of capital still further.

The sad reality is cheaper money won’t work. Individuals aren’t borrowing because they’re still under a huge debt load. And as their homes drop in value and their jobs and wages continue to disappear, they’re not in a position to borrow. Small businesses aren’t borrowing because they have no reason to expand. Retail business is down, construction is down, even manufacturing suppliers are losing ground.

That leaves large corporations. They’ll be happy to borrow more at even lower rates than now — even though they’re already sitting on mountains of money. But this big-business borrowing won’t create new jobs. To the contrary, large corporations have been investing their cash to pare back their payrolls. They’ve been buying new factories and facilities abroad (China, Brazil, India), and new labor-replacing software at home. If Bernanke and company make it even cheaper to borrow, they’ll be subsidizing a third corporate strategy for creating more profits but fewer jobs — mergers and acquisitions.